How to achieve it in the era of distributed energy

David J. O’Brien, Vice President of Regulatory Solutions for BRIDGE Energy Group, works regularly with utility executives to define long-range goals in the context of energy policy and business strategy.

Equilibrium. It's something we often seek, but rarely achieve.

I can recall my college economics professor expounding on the laws of supply and demand - twin contending forces locked in a continual state of seeking equilibrium. I think about this notion often with regard to investor-owned utilities and their regulators. Are we in a place where these two forces are balanced, when both are able to say that their interests and needs are being met? Just like supply and demand, the circumstances for utilities and regulators change over time. Each must assess how well the relationship has adjusted to conform to present needs.

Over the decades of state regulation of distribution utilities, we have seen prominent structural changes - independent power and restructuring - that have altered the basis of the regulatory bargain. Today we stand at another critical point: where the structural underpinnings of the regulatory compact have shifted and a state of disequilibrium exists.

The utility today and the environment in which it operates look vastly different from the days of Sam Insull, when the fundamentals of the regulatory system were formed. Utilities, whether restructured or vertically integrated, can no longer claim to be the sole solution for customers. In 2015, the maturation of energy efficiency and customer-sited generation threatens core utility revenues. Meanwhile, as public sentiment warms towards the environment, renewable supply, and a tech-driven society, we see raised expectations for utilities in terms of reliability, quality of service, and innovation. Unfortunately, what has not kept pace is a regulatory system that determines the nature of utility investment and the means of cost recovery.

These changes cannot be denied. The utility business surely stands in the midst of a structural shift. Core revenues are deteriorating due to a sustained decline in customer load. And that is occurring as a function of energy efficiency, third-party competitors, and consumer self-supply options, such as rooftop solar. At the same time, the increased activity at the grid edge and two-way power flow has caused the grid-operating environment to become increasingly complex and challenging to manage.

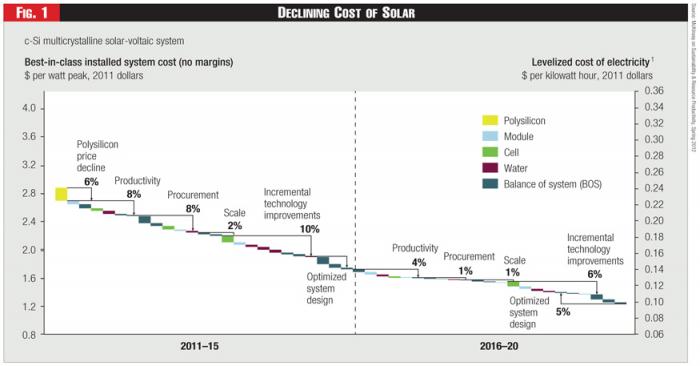

Figure 1 - Declining Cost of Solar

Figure 1 - Declining Cost of Solar

In the emerging era of distributed energy resources, we will find the distribution utility increasingly in the role of an integrator and enabler - more than their longstanding role as energy provider. Accordingly, the regulatory approach must go through its own structural shift to keep pace and restore the system to regulatory equilibrium.

Evolving Business Models

Let's look briefly at the rise of four industry trends and their effects on the traditional utility business model: 1) end-use energy efficiency, 2) third-party product competitors, 3) advanced grid infrastructure, made possible by American productivity growth that occurred during the 1990's, and 4) the declining cost of distributed generation. All four trends lead to rising customer sophistication and expectations.

The end-use energy efficiency programs that were first launched in the 1980's to introduce a demand-side response to ever-increasing energy consumption have reached full maturity in the past decade. In 2013 $6.9 billion was budgeted for energy efficiency programs - up from $ 2.7 billion in 2007, reflecting an average annual growth rate of 18 percent.1 As spending on electric efficiency has risen dramatically over the past decade, it has exerted a profound impact on total electric consumption, with 126 million terawatt-hours (TWh) of electricity saved by 2012. Today, in 2015, efficiency standards have expanded dramatically, with Energy Star appliances now commonplace. Energy efficiency has become part of the culture. Today's consumers look to purchase efficient appliances, light bulbs, and home energy devices, such as intelligent thermostats. As a result we see a considerable impact (downward) on the overall consumption of electricity, putting pressure on traditional utility revenues.

Yet while energy efficiency has proven very effective at reducing overall consumption, it has not slowed the steady increase in peak demand. And since the capacity of the system must be sized to meet the peak load factor, we find that capacity utilization on the electric grid has been steadily deteriorating since the 1980s. Optimizing the use of the grid to improve capacity utilization remains a challenge, as underscored by New York Public Service Commission in its REV initiative (Reforming the Energy Vision).

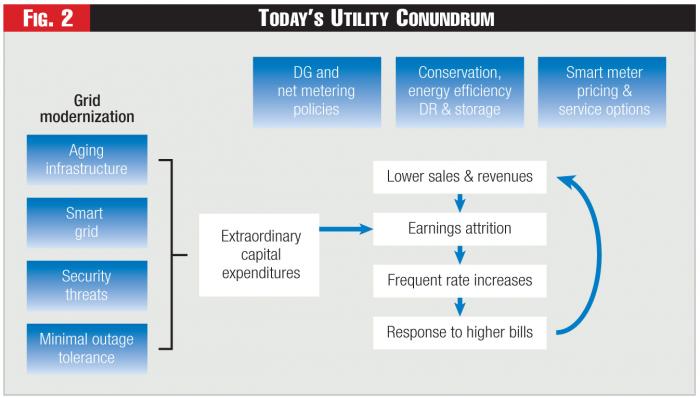

Figure 2 - Today’s Utility Conundrum

Figure 2 - Today’s Utility Conundrum

Consumers are becoming more in tune with energy efficiencies and also accustomed to user-friendly technologies such as smartphones, tablets, etc. As a result, we see today a major expansion of third-party consumer devices that help residential customers use energy more effectively and efficiently. On a trip to Home Depot or many other retailers, you will find a plethora of new products to help automate a home or business. Consumers can now purchase off-the-shelf products that will automate their home thermostat, lighting, locks, garage doors and more.

The emergence of the Nest Learning Thermostat offers a perfect example of a present-day innovation that connects customers to their home meters. The Nest is not only an automated device, but also an intelligent platform that learns from usage patterns and then automatically adjusts the temperature in the home. The device is Wi-Fi enabled and can communicate with customers' smartphones or tablets to enable automated demand response.

In the 1990s, the presence of global competition caused the industry to respond to cost and quality pressures in order to remain viable. Thanks to broad and deep investment in IT, the American economy significantly eclipsed its global competition in productivity growth.

Thus, over the past decade, a new set of digital and IT solutions has emerged in the electric utility industry. Utilities nationwide are increasingly implementing such solutions as advanced "smart" meters, digital grid sensors, communications networks, and data analytics. These new technologies meet the enhanced capability utility operators need to manage a more complex grid and meet the increasing expectations of customers.

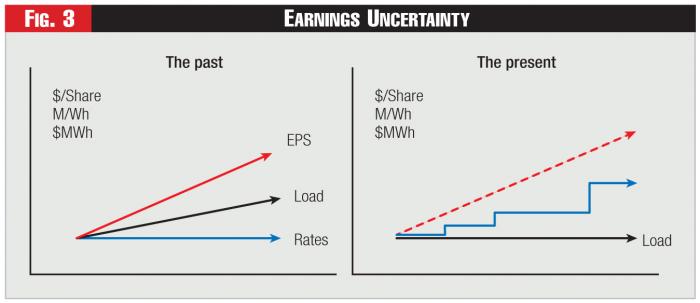

Figure 3 - Earnings Uncertainty

Figure 3 - Earnings Uncertainty

Lastly, we come to distributed generation, which only now is coming into its own.

While there has been an impassioned cadre of supporters of a distributed grid since the 1970s, generally speaking, distributed generation was viewed as a novelty, with energy production priced at a premium but actual production representing an insignificant portion of total energy supply.

In recent years, however, that picture is beginning to change, thanks to persistent global financial subsidies and research and development that has improved the technology and lowered the cost of output. In Europe, Germany stands out in this regard with solar comprising 50 percent of total generation. More and more, it appears grid parity may become a reality.2

This rapid penetration of technology into our daily lives has led to increased customer expectations - expectations that will increase steadily as customers avail themselves of non-utility solutions such as Nest Learning Thermostats, Solar City rooftop photovoltaic systems, and more. The continued success of Tesla Motors forms part of this emerging picture as Electric Vehicles (EVs) become more viable. Residential-level electric storage may be just around the corner with Tesla's Powerwall launch. If that occurs, residential level storage may actually be the smart grid "killer app" that allows residential customers to bypass the grid altogether.

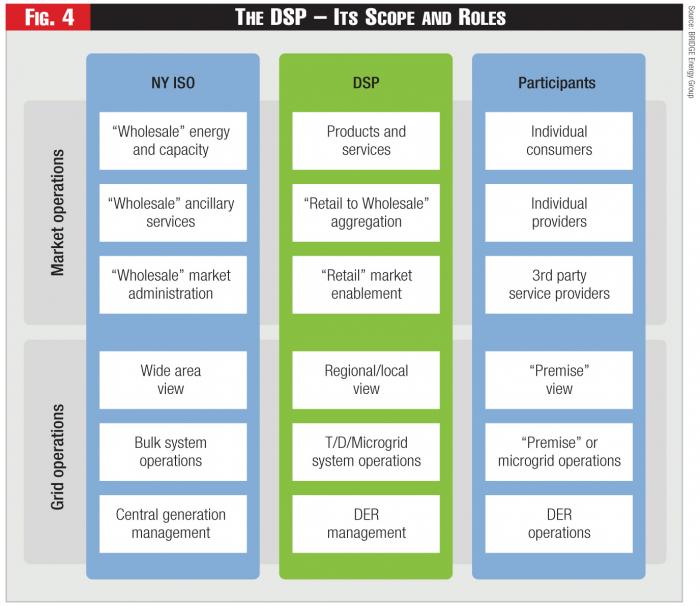

Figure 4 - The DSP – Its Scope and Roles

Figure 4 - The DSP – Its Scope and Roles

Figure 2 visually represents these macro drivers and their impact on the electric utility business model. Revenues are declining while fixed costs remain largely constant, leading to rate increases in order to maintain the revenue requirement.3 As rates rise, customers are keener to look at alternative supply options, especially as the cost of distributed systems fall. This dynamic has been playing out over time and, while not dramatic in most jurisdictions, it has made a substantive effect in some states such as California and Hawaii. What further complicates matters is that many utilities still need to invest in their core network to replace aging infrastructure and incrementally add elements of advanced infrastructure to meet increasing expectations. Thus we have what can be described as extraordinary capital demands at a time when core revenues are eroding.

A Growing Disequilibrium

Traditional least-cost ratemaking principles worked well for an industry marked by a vertically and centrally integrated infrastructure, where demand for electricity and utility revenues tended to outstrip the cost of system investment.

In the heyday of the Insull model, system investment could be accomplished with minimal to non-existent rate pressures. Investor-owned utilities could recover costs and earn a competitive return for shareholders. Utilities prospered by keeping spending low, so as to adjust rates infrequently. Long pauses between rate cases were seen as the best means to institute operational and capital efficiency.

Figure 3 illustrates earnings uncertainty - the contrast between (A) the past , with its steadily increasing load, stable rates, and rising earnings per share, and (B) the present, with load eroding, creating a less-predictable outlook on rates, plus real uncertainty for utility earnings.

Historically speaking, any delay in updating retail rates (regulatory lag) was not a material issue, as growth in sales made it possible to pay for new system investments, even while growing earnings. In 2015 the circumstances are dramatically different. Regulatory lag has become a major issue. As an industry that relies heavily on private capital to fund investment, long-run uncertainty regarding utility earnings and enterprise value is a very real concern.

The lag-oriented regulatory system also presents a fundamental competitive barrier for incumbent utilities because it severely limits adaptability and response to evolving customer expectations. While unregulated, third-party competitors can offer new products and services at their whim, to respond to customer preferences, utilities must file petitions with state regulators and wait for the conclusion of lengthy commission proceedings.

As a result, the traditional regulatory framework is an analog system operating in a digital world. A multi-faceted and dynamic marketplace has developed while the incumbent utility remains in a fixed and regimented environment. Public policy and market maturity have changed the competitive landscape but the incumbent utility is not reasonably allowed to respond. The least-cost regulatory system is slow to adapt, and focused entirely on cost inputs instead of outputs and value creation.

A 'Vision' for Tomorrow

The operating and investment profile of a distribution utility will need to adjust to these structural trends. With the long-run change in demand, and increased customer self-supply, the distribution utility will be marked by how it fosters customer choice and market activity, rather than as a seller of commodity or even a business that delivers electricity from generation to load. In a rapidly evolving and technology-rich industry, with improving solutions to gather information in real-time from grid devices and customers, the utility's value-added role will transition to the operator of an intelligent network. The profile of the Distributed System Platform (DSP) that is being pursued in New York's REV proceeding, or the Distributed System Operator (DSO), common in Europe, offer helpful ways to think about the business model of an Intelligent Network or "Smart Integrator."

For our purposes we will refer to this new business profile as the "platform." In this scenario, the owner and operator of the distribution grid sits in a very critical position in the system between customers and the wholesale market and bulk system.

The New York proceeding, with its concept of the DSP, stands as instructive. The DSP operates as the critical enabling platform that lies between participants in the electric system, end-user customers, third-party solutions, and the bulk system and wholesale market.

Figure 4, developed by BRIDGE Energy Group and the New York Joint Utilities, illustrates the scope and roles of a DSP in a REV-driven electric system. The DSP as the platform in this example retains its traditional grid operations role, while adding new responsibilities to "animate the market."

As shown in the figure, financial, power, and data flows will move across the vertical domains of the DSP, the market participants, and the New York ISO (the independent system operator for the state's bulk transmission grid). In this environment, the utility value equation will be based on building and operating an enabling platform that leverages advanced infrastructure to integrate distributed energy resources, or DERs. The utility role is to provide the physical foundation that fosters a marketplace environment at the distribution level and where the growing third-party solutions for customers can be developed and matured. The aforementioned home automation category serves as a perfect example of the sort of market development that the platform can foster over time.

The use of the term "enable," however, should not give the impression that the role of platform provider is a lighter assignment for the distribution utility. The proliferation of dynamic resources at the edge of the system will present numerous operational and technical challenges as the level of two-way power flow reaches critical mass. The system as we know it today was not built for this operating environment. And so the basic topography of the grid will change. Fortunately, the broad suite of smart-grid hardware and software available today can play a pivotal role by providing dramatic improvement in operational intelligence, automated switching and resource management. Advanced metering infrastructure (AMI), high-speed communications and advanced distribution management systems (ADMS) will continue to play a prominent role.

While the new dynamic environment develops, core utility responsibility for safe and reliable service, will not change. The expectations for reliable electric service are ever increasing in the digital age and given the new complexity of DER, utilities will need to leverage their modern grid capabilities to meet societal expectations. Today reliability is not just about the System Average Interruption Frequency Index (SAIFI) or Customer Average Interruption Duration Index (CAIDI). Rather, customers now expect immediate availability of outage information via diverse channels, efficient restoration of service, and a rock-solid Estimated Time to Restore (ETR). Soon the days of utility personnel calling customers or "looking for porch lights" to see who has service, will be long gone.

A New Regulatory Compact

This new dynamic platform will not be achievable without a modern regulatory compact that provides flexibility and clarity of direction based on an alignment of objectives and where innovation is embraced. The advancement of technology and its means to provide value requires an environment of innovation where trial and error can be undertaken to find the optimal solutions. The most viable means to create such a culture is to establish a performance or outcome-based regulatory framework. At the same time, however, regulators must update the way in which fixed costs are recovered through rate design.

In the U.S., the notion of a modern form of PBR (Performance Based Ratemaking) is largely in the discussion stage. A good example is the "Utility of the Future, Today" or UOF framework that BRIDGE Energy Group introduced in Massachusetts Department of Utility Control investigation into Grid Modernization (DPU 12-76).

UOF represents a dynamic platform where revenues and rates are not arbitrarily fixed, but instead are allowed to float, based on the level of spending year-to-year and adjusted for quality of performance. Utilities, meanwhile, are expected to develop capital spending and asset improvement plans that are directly linked to stated policy goals, system condition and customer demands. Base rates are projected forward based on the approved capital plan but are reconciled annually with actual investment.

Performance lies at the heart of the model and is managed by establishing qualitative and quantitative metrics. The focus shifts from static cost minimization to enhancement of value. The year-to-year review of outcomes is a counter-weight to skepticism of the value equation and visualization of the progress of innovation. Metrics also greatly enhance transparency and accountability on the part of the utility, which goes directly to regulatory concerns regarding the prudency and value of capital investment. This new PBR model was influenced by the RIIO approach utilized by the Office of Gas & Electricity Markets (OFGEM) in the United Kingdom and by the EIMA legislation passed in Illinois in 2011.4

Modern performance based rate approaches are the means to reach a new "regulatory equilibrium". The ratemaking approach shifts to a more real-time recovery of costs, providing greater clarity and earnings potential for utilities and their investors. In return, the utility is more accountable for outcomes than ever before and with greater transparency into their capital spending and operations. These are principles that can form the foundation of a new regulatory compact.

Endnotes

1. Summary of Electric Utility Customer-Funded Energy Efficiency Savings, Expenditures, and Budgets: Issue Brief, Edison Foundation Institute for Electric Innovation, March 2014, prepared by Adam Cooper and Lisa Wood.

2. Grid parity refers to a point at which the cost of alternative resources like solar will be equal to the cost of grid delivered energy. There are some jurisdictions where that has already occurred such as Hawaii and will soon be the case in California.

3. The addition of DERs (distributed energy resources) is not eliminating customers' need to access the grid and have access to electricity throughout the day. As a result the capacity of the grid and the cost to run it remains largely unchanged. Therefore the revenue requirement of the utility is not reduced, necessitating rate increases to maintain the revenue requirement.

4. RIIO (Revenue=Incentives + Innovation + Outputs) framework administered by OFGEM, the national regulator in the United Kingdom. See, "A Trip to RIIO in Your Future?" by Peter Fox-Penner, Dan Harris, and Serena Hesmondhalgh, Public Utilities Fortnightly, Oct. 2013, p,. 60. EIMA, Energy Infrastructure Modernization Act set forth a long range approach to grid modernization investment with forward looking rate setting and performance metrics.

Lead image © Can Stock Photo Inc. / valex113