Distributed energy has a long history in the state – with co-generation, or combined heat and power, playing the dominant role. How is that portfolio changing today?

Hugo van Nispen is executive vice president of the global Energy Advisory business at DNV GL, a leading energy consultancy and one of the world’s top testing, inspection and certification bodies, and is the primary architect of the energy industry’s leadership forum – Utility of the Future (http://www.dnvgl.com/news-events/events/U-of-F-2015.aspx). Previously he served as president and CEO of KEMA, Inc., guiding that company through its merger with DNV Cleaner Energy – the deal that formed the current DNV GL.

CHP has fueled New York State's economy - and shaped the famed skyline of New York City - since 1881. That was the year New York Steam, a predecessor of Consolidated Edison, completed construction of the first central steam plant, consisting of 48 boilers located at Cortlandt, Dey, Greenwich and Washington Streets. Its 225-foot chimney was the second tallest structure in the city, just below the spire of Trinity Church. The distributed energy system, producing electricity and heat, grew along with the city in the 20th century, making possible the elegant smokestack-free profiles of art deco giants like the Chrysler Building, Rockefeller Center, and the Empire State Building.

Today, CHP (combined heat and power) still comprises the majority share - 57 percent - of the state's distributed energy resource (DER) portfolio. It's an effective distributed resource that has endured, but what role will it play as the state drives toward a smart energy future in an era of aging infrastructure, superstorms and regulatory uncertainty?

In 2014, the New York Independent Service Operator (NYISO) commissioned global energy consultancy DNV GL to assess the role and potential for distributed energy resources in the state. Its aim was to examine the current and potential roles of distributed energy in the ISO region. The study, referred to herein as the "2014 DER Study," provides an extensive examination of the complex forces at work in developing the economic, technical, and regulatory aspects of a grid integrated with distributed energy resources. It also documents CHP's central role, finds a surprisingly robust solar presence, and examines the characteristics needed for any particular distributed resource to contribute to a reliable, clean, economically viable grid.

Find the full August 2014 DER Study, "A Review of Distributed Energy Resources," by DNV GL, at the NYISO or DNV GL websites.

CHP in Today's Portfolio

The pioneering Con Edison CHP system remains in operation today as the largest district heating system in the United States "using waste heat from both electric generators and dedicated steam facilities to provide space heating and cooling" according to CEERE (Center for Energy Efficiency and Renewable Energy), located at the University of Massachusetts at Amherst.

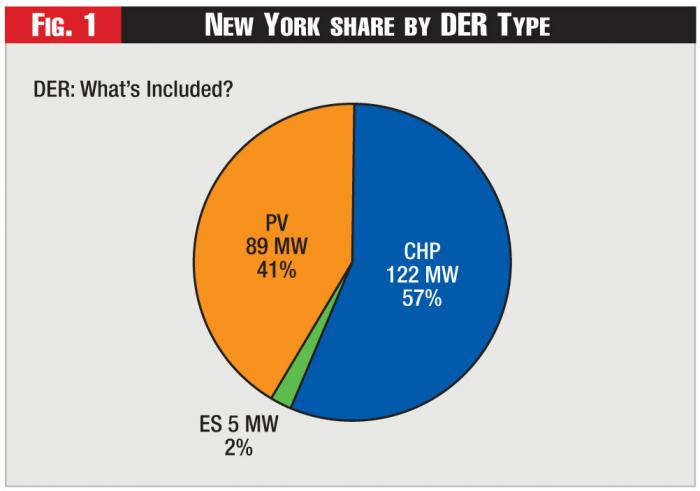

Figure 1 - New York share by DER Type

Figure 1 - New York share by DER Type

Con Edison's online history page notes that it has "105 miles of mains and service pipes, providing steam for heating, hot water, and air conditioning to approximately 1,700 customers in Manhattan." Yet according to a 2011 report from ACEEE (American Council for an Energy-Efficient Economy), it is New York City, where CHP first took root, that presents "the biggest barriers to CHP in the state, where real estate prices and Con Edison's old networked grid present financial and technical difficulties."1 Nevertheless, it is the state's CHP regulatory climate, along with incentive programs and support from utilities like National Grid and organizations like the New York State Energy Research and Development Authority (NYSERDA), that have kept CHP attractive.

New York's current DER generation portfolio consists of 122 MW (57 percent) CHP, 41 percent (89 MW) solar PV, and two percent (5 MW) energy storage. Figure 1 shows the current dominance of CHP in New York's installed DER resources.

"Distributed energy resources" can mean many things. For example, the New York Public Service Commission's influential REV report, "Reforming the Energy Vision," includes energy efficiency and demand response resources as DERs. For the DER Study that is the subject of this article, DER technologies were defined more narrowly to refer to "behind-the-meter" power generation and storage resources - typically located on an end-use customer's premises - that supply a customer's electric load. This definition includes technologies like solar photovoltaic (PV), microgrids, wind turbines, micro turbines, back-up generators and energy storage. These resources may also be capable of injecting power into the transmission or distribution system or into a non-utility local network in parallel with the utility grid.

In addition, the term "behind-the-meter" here means resources not connected on the bulk or wholesale electric power system, but connected behind a customer's retail access point (the meter). These resources may be serving the customer's internal electric loads or selling capacity into the bulk electric power system.

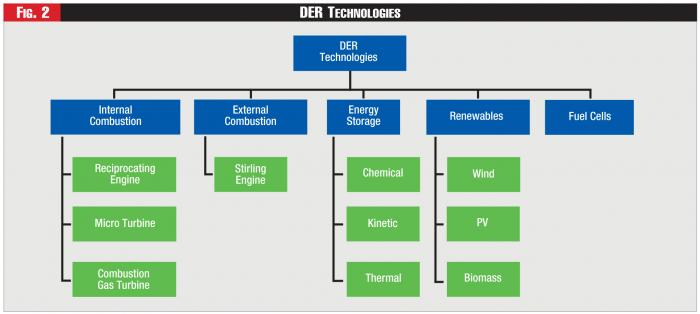

Figure 2 - DER Technologies

Figure 2 - DER Technologies

CHP is not the only legacy resource with a long history, wide market penetration, and known economic factors. Combustion engines represent another DER type with these characteristics. Internal combustion engines, including the reciprocating engine, micro turbine, and combustion engine, as well as external combustion engines like the Stirling engine, remain in use today. New DERs, whose adoption and economic factors are less well established, include renewable generation, including wind, solar, and biomass. Energy storage is another capacity resource and may take the form of chemical, kinetic, or thermal technologies. Whether new or old, each is capable of producing power to support the host load or the grid. Each is evolving and being adopted at its own pace, bringing new challenges to the planning, operations, and market administration of New York. Figure 2 illustrates the types of DERs considered under this study in addition to CHP.

New York vs. Other States

DER adoption around the nation is growing in much the way New York's has - from each region's unique history and resources. Some technologies experience greater penetration around the country due to physical or indirect market conditions creating more potential. Just as New York has access to significant CHP infrastructure and knowledge, other states have significant advantages in geothermal or solar resources. Policy conditions factor in, too, particularly where regulators lower barriers to entry or explicitly encourage adoption through incentives.

In terms of cumulative adoption of the three resources that dominate New York - CHP, solar PV and energy storage - California, New Jersey, and Arizona lead the nation in deployments of two megawatts (MW) or lower. Figure 3 illustrates market penetration estimates for the ten states with the greatest penetration. Large amounts of PV in these states drive the high overall DER penetration, with PV constituting over 80 to 90 percent of the total installed DER capacity for units less than two MW.

New York ranks within the top five states, but is unique in having a portfolio in which CHP technology leads total DER penetration. CHP contributes 57 percent of New York's DER capacity. Solar is the second contributor in New York and by some estimates of installed PV capacity, New York has roughly 100 MW more PV than is reflected in the NREL Open PV Project database (at the time these numbers were derived). The size of the installed capacity, however, was unknown, making it difficult to adjust estimates for total capacity under 2 MW. It is feasible that the installed capacity of PV and CHP sites less than 2 MW are now roughly equivalent and that the total installed capacity in New York of DERs under 2 MW is now greater than 216 MW.

Figure 3 - DER Adoption by State

Figure 3 - DER Adoption by State

Figure 4 illustrates the leaders in each resource type (whereas Figure 3 showed total capacity by state). It highlights states with the top ten installed capacity of units 2 MW or under per type of DER. California, New York, and Pennsylvania lead across states with the top PV, energy storage, and CHP capacities under two megawatts.

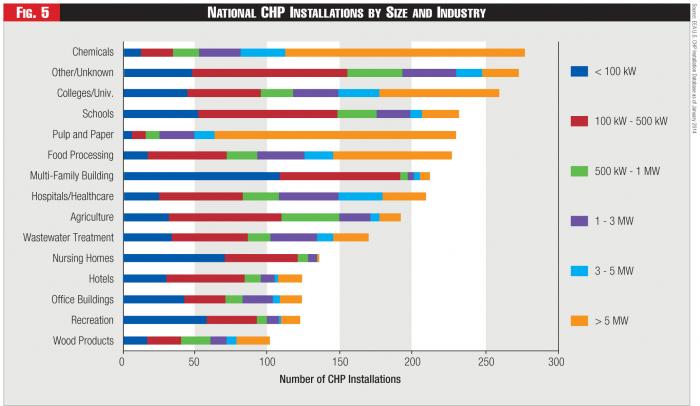

In terms of size of distributed generation capacity, CHP resources tend to be larger than many other distributed sources. In New York as well as across the U.S., the vast majority of CHP units in use today are greater than 5 MW, as illustrated in Figure 5. However, ACEEE notes that new technologies are making smaller units more cost-effective: "New turbines are now cost effective for systems down to 500 kW and reciprocating engines for systems down to 50 kW, dramatically expanding the number of sites where CHP can be installed."

The DOE's Combined Heat and Power Installation Database includes a large voluntary record of CHP deployments. It reveals that the majority of installed CHP capacity consists of combined-cycle CHP units. However, the majority of smaller-scale capacity is comprised predominantly of microturbines and reciprocating CHP engines. All CHP technologies, including combined-cycle units, microturbines and reciprocating engines, are well-developed technologies.

The Optimal DER Portfolio?

For any DER to succeed, it must meet certain characteristics - among them responsiveness, affordability and reliability. The 2014 DER Study assessed the qualities of leading DER resources extensively. This article provides an overview, including a glimpse of how CHP compares to other resources.

Figure 4 - Energy Market RiskStates with Top 10 Ranking in DER Adoption by Type

Figure 4 - Energy Market RiskStates with Top 10 Ranking in DER Adoption by Type

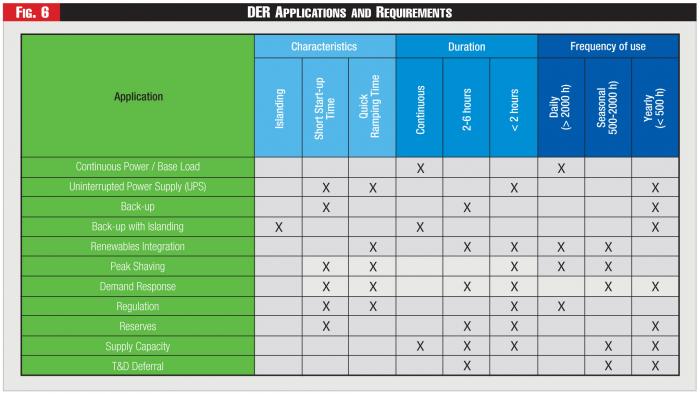

DERs can serve a number of applications, each of which has their own performance requirements. For example, participation in NYISO's Special Case Resource program requires a two-hour ramp period whereas regulation services require, effectively, instantaneous ramping. Figure 6 provides a high-level outline of duration, frequency and start-up and ramping requirements by application.

DER performance, characteristics, typical sizing, and associated fixed and operational costs vary quite widely. For example, start-up times can range from milliseconds to minutes depending on the technology. Figure 7 outlines typical ranges of size, cost, and performance characteristics across engines (including CHP technologies), fuel cells, storage, and PV to provide a sense of the variation of DERs. Ranges can be broad due to variance in performance under different conditions (such as ambient temperature, fuel make-up, etc.) and due to different levels of optimism about technology capability. View a large pdf of Figure 7 here.

The CHP resources evaluated here under the category "Internal Combustion Technologies" tend to be fairly nimble - with a ramp time of about 10 to 15 minutes (compared to three or more hours for several of the fuel cell types) and the capability to operate at fairly high heats and to provide a wide range of power "size" (from 30kW to 6+MW). Clearly, there is no one "best" resource for all use cases; only a set of best options for each individual use case.

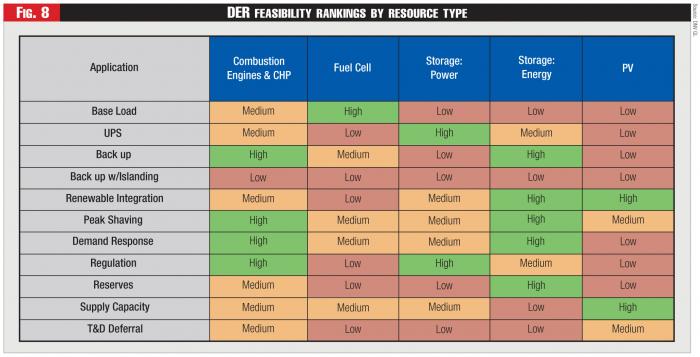

Pairing DER technologies and economic characteristics with application needs provides an indicator of how different DERs might be suited for different applications. Figure 8 provides a high-level overview of application feasibility, based on typical load profiles and capabilities or needs of technologies and applications. Actual installations will depend on the specific technologies being used, the specifics of the application for which a DER is being used, and other non-DER-related factors, such as available incentives or relevant policies.

Figure 5 - National CHP Installations by Size and Industry

Figure 5 - National CHP Installations by Size and Industry

For New York, as for other markets, best DER technologies will need to be determined on a case-by-case basis, as shaped by individual needs and resource characteristics, as well as the regulatory climate.

Resource Cost Improvements

CHP has seen enhancements in recent years, but costs generally have not come down as rapidly as other technologies like PV and energy storage. However, the market for CHP is likely to grow through an increased focus on resiliency and continued financial and educational outreach supported by state and federal programs.

Energy storage and PV technologies have both improved their cost-effectiveness and performances in dramatic fashion over the past two decades. According to the Solar Energy Industries Association, the national average installed price for residential and commercial PV systems dropped by 31 percent from 2010 to 2014, with a reduction in New York of 4 percent within the last year. Recent advancements in energy storage have also been strong. For example, lithium-ion batteries have doubled their energy density over early versions and are ten times cheaper.

Costs are expected to continue to drop. Many in the industry believe there is opportunity to reduce non-module PV costs. In 2013, NREL (National Renewable Energy Laboratory) released a roadmap to reduce non-hardware ("soft") costs by 2020, with targets of $0.65/W and $0.44/W for residential and commercial systems, respectively. Private and public investment in additional research and development in PV and energy storage is strong. DOE incentives like the SunShot Initiative aim to lower residential and commercial installed costs of PV systems to $1.50/W and $1.25/W respectively by 2020. The Joint Center for Energy Storage Research, a public-private research partnership managed by the DOE, has set a cost reduction goal of $100/kWh for stationary storage with a life of 20 years and 7,000 cycles and a round trip efficiency of 95 percent.

Figure 6 - Wholesale Power Price Changes ($/MWh)DER Applications and Requirements

Figure 6 - Wholesale Power Price Changes ($/MWh)DER Applications and Requirements

Microgrids, though they have existed on naval and sea-going vessels for nearly a century, are a recent phenomenon in the electric grid. According to GTM research, there are 81 microgrids operational today and 35 more are planned. The New York Public Service Commission (PSC), NYSERDA, and the state Department of Homeland Security and Emergency Services are currently conducting a feasibility study of microgrids in New York to assist with disaster response. The New York State Smart Grid Consortium is also compiling a database of microgrid projects in New York State.

Fuel cell markets are currently growing in stationary applications globally, though domestic growth rates are much slower. Shipments of stationary fuel cells grew from about 2,000 shipments in 2008 to about 25,000 shipments in 2012. However, most of the market growth is abroad rather than domestic. Nevertheless, investment in fuel cells in the United States has been relatively strong and research continues. U.S. investors made the largest cumulative investment globally in fuel cells between 2000 and 2011, at $815 million. Though federal research budgets for fuel cells have declined somewhat in recent years, funding continues. Department of Energy goals for stationary fuel cells by 2015 include a $750/kW cost target with 40 percent efficiency and 40,000-hour durability.

Regulatory Policy

The challenge in assembling a DER portfolio is the difficulty of ensuring economic success when the regulatory policies and market drivers and incentives are unknown, uncertain, and likely in flux. DERs could make everything better, or really botch things up, depending on a huge array of circumstances often outside the control of those who must select and deploy the resources. It is a daunting task and the 2014 DER Study examines some of the most important factors the state will need to consider in building a successful program.

Consider the question of incentives, which can help align the goals of both the customer and the grid operator.

Figure 7 - DER Technology Characteristics

Figure 7 - DER Technology Characteristics

The nature of DER benefits depends greatly on the mix of DERs on the grid and on the ability to coordinate DER activities in a way that aligns individual customer interests with grid interests. Grid owners and operators may have reason therefor to incentivize certain types of DER adoption and behavior on their respective systems. For example, by offering incentives, transmission and distribution owners and operators could potentially motivate investment in particular locations or shift in operations to align customer benefits with grid benefits. That could potentially result in the ability to defer investments in distribution, transmission or generation capacity. Alternatively, incentives could motivate a shift in operations or location or investment in certain types of DERs or integration equipment. Operational savings might include power system loss reductions or avoided energy purchases. The benefit of avoided energy depends on alternative costs for supply, which can vary by time of day.

Also, customers may encounter a number of mixed economic signals - from their load serving entity, wholesale operator, and local and federal governments. Retail rates, including energy, demand and standby charges, can influence DER operations and investment by providing incentives to reduce peaks and establishing a basis for comparison of per-unit production.

For example, rate structures can vary, including fixed, variable or a combination of the two, which will also likely influence DER operations from an economic perspective. A variety of retail rate offerings are available in New York, ranging from fixed charges to time-of-use charges to mandatory hourly pricing. Two such offerings are net metering rules and feed-in tariffs.

State net metering rules define the eligibility requirements, size, capacity, and prices for DER that can be offset or sold back to the grid at retail rates. The number of customers in the United States with net metering has steadily grown over the years. According to data collected by the EIA since 2003, the number of customers with net metering has grown forty-eight-fold between 2003 and 2012. The majority of net metering applies to PV units. Based on 2012 data from the U.S. EIA, New York ranks within the top ten states in terms of the estimated amount total capacity that is priced through net metering.

Figure 8 - DER feasibility rankings by resource type

Figure 8 - DER feasibility rankings by resource type

Some utilities in the United States have implemented alternative approaches to net metering for compensation of excess production. For example, Austin Energy has implemented a Value of Solar Tariff. Rather than applying net metering, Austin Energy bills customers at the full retail rate for their load and separately credits them the determined 'value of solar' for each kWh they generate.

Feed-in tariffs (FITs) are used in portions of the United States, including New York. These tariffs typically guarantee customers who own eligible generation a set price from their utility for all of the electricity they generate and provide to the grid. Currently, the Long Island Power Authority runs a CLEAN Solar Initiative FIT. Its latest iteration had a cumulative program target of 100 MW.

Interconnection Complexities

The interconnection process, and all the various related technical, contractual, metering, and rate rules, defines the process by which a generator connects to the grid. The authorities overseeing this process and the manner in which they treat resources can depend on several factors:

• Point of interconnection. Whether the assets are connecting directly into the transmission grid (which is regulated by FERC, the U.S. Federal Energy Regulatory Commission), the distribution grid (which is not FERC-regulated), or behind the customer meter.

• Asset Size. What the planned capacity is that will be interconnected.

• DER Application. Whether the unit produces excess power, and whether and how it plans to interact with the wholesale market.

Generally, procedures for interconnection will vary, depending on whether resources are on the utility side of the meter or behind the meter. The Standard Interconnection Requirements procedures in the State of New York were recently updated (February 2014) by the PSC for a more transparent and swift process for distributed generation below 2 MW. A "fast track" application process is available to distributed generation below 50 kW, or to inverter-based generators (such as PV) below 300 kW, with some exceptions such as underground interconnections.

Government Incentives

Government incentive programs may exist at the federal, state, or local levels.

Federal incentive programs are generally geared towards supporting state or local governments in reaching their energy, efficiency, and development goals by providing grants and loan guarantees to eligible projects. A portion of these incentives are aimed at rural communities and combine goals for economic development and environmental protection. There are also incentives structured as corporate and personal tax incentives. While many incentives may apply to DER indirectly, the federal business energy investment tax credit, the Rural Energy for America Program and residential renewable energy tax credit are examples of programs more directly tied to DER installations.

There also may be multiple incentive types and programs available at the state and local levels.

In states with Renewable Portfolio Standards (RPS), many utilities are required to procure renewable energy to meet certain targets. In some cases, there are special carve-outs for distributed generation. In total, 29 states have RPSs and 16 of these states have carve-outs for solar or another form of distributed generation. The PSC adopted an RPS for New York in September 2004. In its current implementation, the RPS sets a target of 30 percent of state electricity consumption from renewables by 2015.

Several other state and local incentives may be relevant to DERs. For example, the Property Assessed Clean Energy financing initiatives provide an innovative way to finance renewable energy upgrades to buildings via property tax assessments. In addition, many states offer tax incentives geared towards renewables (typically PV) and energy efficiency (including CHP), such as sales tax exemptions and corporate tax credits.

This year, the PSC has launched an initiative, Reforming the Energy Vision (REV), to engage end-users, promote efficiency and wider use of distributed resources, and meet the challenges of aging infrastructure and severe weather events. The PSC Chair, Audrey Zibelman, has outlined a goal to decentralize the grid and engage consumers, allowing DERs to play an active role in grid management. Seventeen proceedings are currently underway.

In addition, in January 2014, the State published a draft State Energy Plan, describing several new and on-going initiatives, policies, and programs to meet State and local energy goals. Several initiatives are pertinent to DERs.

In support of state policy objectives, NYSERDA administers several incentive programs targeting renewables, energy efficiency, and sustainability. Sample programs related to DERs include:

- Solar PV Program Financial Incentives;

- Solar Thermal Incentive Program;

- CHP Performance Program; and

- CHP Acceleration Program.

In addition to statewide initiatives, several cities within New York have energy plans in place or under development. For example, in 2011, the City of New York published a city energy plan with the explicit goal to "build a greener, greater New York by reducing energy consumption and making our energy supply cleaner, more affordable, and more reliable." Many of the goals outlined in the plan can be addressed with DER.

Room for Growth

The remaining technical potential for DERs in the United States is high. And though New York's total installed capacity of DER is relatively high, there is room to grow there as well.

Building from its strong base in DER rooted in CHP, solar could provide additional resources to the state. A recent report by NYSERDA estimates solar could contribute a total technical potential of 881 MW cumulative peak capacity and 2,836 GWh production by 2020, and 2,615 MW cumulative peak capacity and 8,223 GWh production by 2030. For PV serving commercial customers, NYSERDA estimates a total technical potential of 1,174 MW of cumulative peak capacity and 3,706 GWh of production by 2020. It envisions 3,487 MW of cumulative peak capacity and 10,745 GWh of production by 2030.

Endnotes:

1. See, Anna Chittum and Nate Kaufman, Challenges Facing Combined Heat and Power Today: A State-by-State Assessment, ACEEE Report No. IE111, Sept. 2011.

Lead image © Can Stock Photo Inc. / rabbit75can