More than just energy, it's becoming part of the grid.

Richard Fioravanti is vice president for distributed energy resources at DNV GL. He assists utilities, manufacturers, and policymakers with business plans, financial models, and device testing for advanced storage technologies, microgrids, and other distributed energy applications.

REV, also known by its formal name, "Reforming the Energy Vision," marks a bold initiative from New York to help increase the efficiency, reliability, and resiliency of the electric grid across the state. REV essentially re-envisions the state's future grid as a system fueled by wind, solar, and other distributed generation sources, and then enhanced by smart technologies and tools including microgrids, efficiency programs, and demand response. One of the most striking aspects of REV is the unique role it assigns to energy storage.

REV will follow two tracks of implementation and each will examine energy storage. The first track aims to establish a policy approach to encourage technologies, while the second track focuses on the regulatory changes needed to implement it. Significantly, Track 1 defines the role of distribution utilities in the deployment of distributed energy resources (DERs), proposing that distribution utilities should act as distributed system platforms (DSPs) to incorporate assets into grid operations. Ideas coming out of Track 1 already appear to redefine the role of storage in New York, but the significance of these changes will likely resonate well beyond the state.

Part of the Fabric

In its Track 1 decision (Order Adopting Regulatory Policy Framework and Implementation Plan, Case 14-M-0101, Feb. 26, 2015), the New York Public Service Commission (PSC) generally forbade utility ownership of distributed generation. But in the case of energy storage it carved out an exception - an exception that all but swallows the rule. Importantly, the PSC found that utilities may own distributed storage without concern over the competitive implications when it becomes a part of the very fabric of the distribution network:

"Storage technologies integrated into grid architecture can be used for reliability and to enable the optimal deployment of other distributed resources, and we agree with Staff that this application of storage technology should be permitted without the need for a market power analysis." (REV Order, pp. 68-69.)

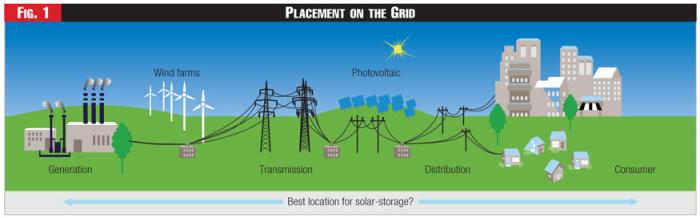

Figure 1 - Placement on the Grid

Figure 1 - Placement on the Grid

The rationale for this exception is rooted in the conviction that energy storage upholds grid reliability and resiliency. Thus, this conviction represents a significant shift in regulatory policy. New York clearly has recognized both the value of energy storage and the broadening of its role in the grid of the future.

Historically, storage has often provided backup power for commercial and industrial applications. Increasingly today, storage integrates renewables - particularly in systems that are enclosed, or "islanded" That's where the lack of flexibility of the grid creates hurdles to integrating large percentages of renewables. And with its fast response capabilities, storage is made to order for frequency regulation - a better alternative to relying on the open market to purchase wholesale energy. In fact, policymakers just now are beginning to adopt storage as a tool to augment reliability and resiliency at the grid level. Perhaps the role of Superstorm Sandy and other extreme weather issues have driven recognition of the need for greater grid resiliency as well as awareness of the role storage can play in providing it.

Reliability and Resiliency

Like New York, other states are beginning to treat energy storage as a reliability asset. Storage-as-reliability applications have appeared among proposals to the California mandate (October 2013) for the state's utilities to procure 1.325 gigawatts of energy storage. In November 2014, for example, Oncor Energy requested regulatory approval for $5.2 billion of storage on the Texas grid to improve reliability. Taken together, the initiatives in Texas and California - and now the New York REV - promise not just another application for storage, but the emergence of storage redefined as a reliability asset.

And the distinction is not merely semantic. With three states treating storage as a reliability tool - one that can be owned or operated by utilities for resilience purposes - a new definition for the technology is taking root. The states are setting precedent, not only among stakeholders, but for regulators as well.

The exception proposed by the state of New York marks a call to action for utilities and all energy stakeholders. The future distributed grid may entail the placement of energy storage at multiple points of the grid. As the storage industry and the mechanisms reach a state of mass deployment, utilities are perhaps the biggest buyers among a large potential pool of customers.

New Uses, New Markets

In the past, utilities may have owned storage mainly for protection, peak shaving or deferral of substation upgrades. Today, with energy storage emerging as a reliability tool, the technology lies within a category of grid assets that carry societal benefits as well as utility benefits. Storage as a rate-based energy storage resource on the utility side of the meter is moving closer to reality.

The extent to which stakeholders can act on this redefining of storage as a reliability and resiliency tool and push storage down this path will depend on market need for storage applications. How much could this be worth? The case of Oncor, the distribution utility based in Texas, provides insight into the potential.

Oncor conducted a study to determine the amount of storage required to improve and provide the reliability levels expected of the grid. In this case, the estimate was for $5.2 billion dollars of storage, spread across the distribution system. This amount was for the entire state, not for a single utility. However, even if 30 percent of that value is dedicated to one of the larger utilities, it is still a significant investment in assets. In addition, the estimate was based on savings and potential revenues that the devices could obtain to offset the cost of the deployment.

Moreover, the Oncor study also examined how to fund and pay for the investment. True, the mechanisms chosen to pay for the investment were unique to the rules and regulations in Texas, where most of the investment in grid assets need to look upstream, from the distribution system to the transmission and generation system. However, the analysis provides a baseline or an estimate of the potential MW size of this application. Oncor proposed this initiative to the Texas Utility Commission and the utility is now working with the commission to help in the understanding of the proposal.

REV and the Market Impact

While in Texas it was the utility proposing storage to the commission, in New York it is the commission offering the proposal to the utilities. Typically, that makes for an uphill battle for utilities to prove the societal benefit of investments to improve operation of the grid. But in New York the commission already understands and supports the societal benefits that energy storage can deliver.

Both scenarios may provide a model for utilities to approach the challenging issues of grid modernization. Across the U.S. and around the world the roadmaps to achieving this goal are just now emerging. And it appears that states are looking for utilities and stakeholders to recommend storage implementation plans to do it.

The challenge is not just to find thought leadership on creating a more distributed grid. Nor is this a debate on whether we will see a greater proliferation of distributed generation. Rather, a distributed grid is the probable, perhaps inevitable, future. Utilities must start mapping their modernization plans and recognize that storage, particularly when viewed as a reliability asset, will be a key component of that modernization. With the initiatives in California, Texas, and now New York, it is not a novel concept to plan for storage being sited on the utility and customer sides of the meter.

In REV and other initiatives, the use cases - and the business case - are becoming clearer.

Some states are building the case for storage as a solution whose benefits are accepted as part of the premise. As storage continues to decline in price, becoming more commercialized and established, these states are forming blueprints for ways storage can be deployed to support the grid and looking to its stakeholders to assist in its quantification. Whether this quantification is in the form of storage being used to support provide reliability and resiliency or is in the form of types of hybrid applications where storage is coupled with solar, or even in hybrid financing mechanisms that involve combinations of public-private mechanisms, the market is ready and asking for these next steps to be taken. Regulators, utilities and storage vendors recognize the value. If the question is, "When should utilities start formulating ideas to begin to map this future?" The answer is simply, "Now!"

(Ed. On July 28, in the REV proceeding, the staff of the New York Department of Public Service released a 135-page whitepaper for public comment that outlines ideas on ratemaking and utility business models. Earlier, on July 1, the DPS staff floated its "BCA" whitepaper on how to analyze and quantify the benefits and costs of distributed resources.)

Only a few short years ago, utilities could view the landscape of storage and continue down a path affectionately referred to as the "do nothing" approach. The thinking was to wait for the technology to mature. Today, however, with solar-plus-storage technology moving quickly to market, clinging to such hopes will put utilities at risk.

The advantages to coupling solar and storage are clear. On its own, solar is a variable device, unable to be used for demand reduction programs or counted as a guaranteed asset during outage events on the grid. However, when coupled with storage, solar becomes dispatchable and can be utilized and counted on for grid operations. The benefits for customers exist as well, as storage can shift excess solar generation to a more opportune time of day and, in the event of a loss of gas and electricity infrastructure, literally provide a perpetual source of energy for critical home loads.

Prior to May 2015, utilities had the luxury of evaluating the potential of this joint application, even contemplating how best to participate in the deployment of solar + storage systems. Tesla's announcement of the Power Wall shifted the debate. No longer was the question "when" or "if" solar + storage could serve as a resiliency tool. Suddenly, deployment was imminent. Tesla is selling the Power Wall and coupling the battery to solar applications, including utility scale deployments. Some residential customers will want to adopt the application, too.

Behind or In Front?

As storage takes root and the technology becomes accepted as a reliability device, the next question is going to be about where to locate the storage device. Market forces and customer desires will answer this question eventually, but the debate need not be an either/or discussion. Compelling reasons will emerge to place storage behind the meter, as well as to place it on the utility side. This issue deserves to be considered, not only based on customer versus utility "wants," but upon what placement of storage will allow the best utilization of the device to improve grid reliability and resilience.

"Behind the meter" is a street term for customer side of the meter (residential, small commercial, industrial) while in this case, utility side refers to the distribution substation. Think of a fence drawn at the meter, where the utility owns all on the "utility" side of the fence and the customer owns all that is in the house on the other side of the fence. The term "behind the meter" affectionately refers to the end use side that the utility doesn't own.

The stakes are high in this debate, with utilities, power providers and developers all jockeying to prosper in a market potentially worth billions. REV and the activities of other states and developers and manufacturers are all accelerating this discussion. Storage can be located at many points on the grid. Even today, individual states are building roadmaps on how storage can access markets either upstream or downstream from their location.

If solar project developers and storage project developers successfully penetrate the commercial, residential, and industrial market, will a utility placing storage at a substation for reliability/resiliency simply prove redundant? Utilities must consider the cost and potential challenges to operating and maintaining the device. Commercial offerings already are shaping the direction of the market. For makers and sellers of storage, how might the location of the storage matter? Would it simply be easier selling to a utility versus an end-use customer? The potential debate will be more than academic.

Forms of Ownership

Under REV, utilities can own storage resources - but should they? What is the business case for ownership? What are the benefits and drawbacks of each? The models for ownership are changing fast and several innovative, even hybrid models have emerged.

Joint ownership may offer one option. Since storage provides value to customers and utilities alike, why not share the assets and technologies? The California Energy Commission brought this question to DNV GL. What if the storage went on one side of the meter and an asset like solar went on the other? This approach makes the storage asset easier to justify economically because it benefits both energy provider and user. Instead of examining the benefits of storage on the utility side of the meter only, and conducting a benefit-to-cost assessment of that application, this shared ownership model advances both sides of the equation.

Beyond shared ownership, what about shared control? These approaches would require regulatory and policy changes, but as New York begins to pioneer innovative approaches and visions to its grid, the potential to implement these concepts may not lie so far away.

How will REV and other state initiatives manage the financial impact of storage under this new definition of storage as a reliability asset? Will they allow storage to be rate-based? Even if the benefits outweigh the cost, can the rate base absorb assets worth billions without raising the cost of electricity? Of course, this discussion applies not just to storage, but to the whole process of modernizing the grid. Innovative hybrid approaches to financing may lessen the cost of adoption. Combinations of utility and customer contributions, public and private financing are all approaches New York and other states may consider.

Point of Decision

The process unfolding in New York is not a "one off" event. It's a pivotal moment across the country for deciding how to define and deploy storage as a grid asset. Today is no time for sitting back and watching the parade pass by. There is significant money on the table. Stakeholders and market forces already are weighing in. All stakeholders - and utilities in particular - should take part and provide the guidance and analysis that the issues require. Providing qualified and quantified analysis will do more than just benefit the utility industry. It will shape tomorrow's power grid and the economy that depends upon it.

Lead image © Can Stock Photo Inc. / buffaloboy2513