Ask What RTO Markets Can Do for Customers

Jay Morrison is an Energy Bar Association Primer Dean and Vice President of Regulatory Issues at the National Rural Electric Cooperative Association. This article does not necessarily represent the views of NRECA or any of its members.

The Federal Energy Regulatory Commission and the electric utility industry are embroiled in several complicated and controversial discussions.

Those critical issues include conflicts between state policy and organized wholesale markets and the role of "self-supply" in RTO capacity markets.

They also include whether RTOs or states should or even may offer support to generation resources for their resilience benefit as well as the right of "relevant electric retail regulatory authorities" to decide which distributed energy resources may participate in wholesale electric markets.

There is a common thread among them. There is a common approach that would allow all to be resolved in a consistent fashion.

They all arise from a recent inversion of the traditional vision of the electric utility industry. They can largely be addressed if we recognize that the inversion is unnecessary, arguably unlawful, and counter to the public interest.

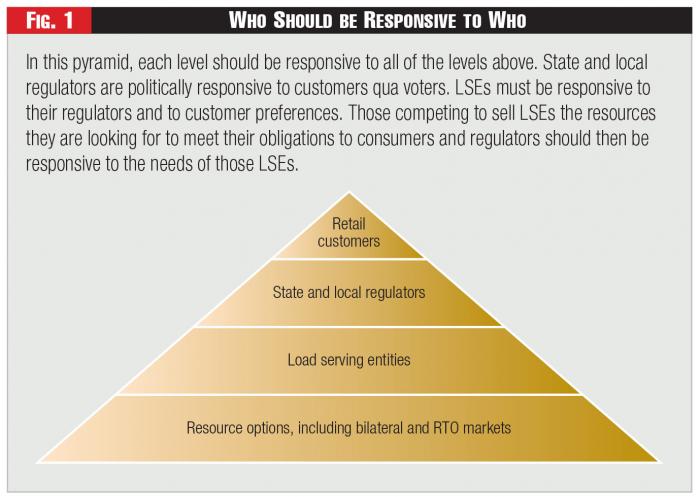

Figure 1 - Who Should be Responsive to Who

Figure 1 - Who Should be Responsive to Who

Since the regulation of electric utility service began in the first decades of the twentieth century, the retail customer has been at the top of the industry's pyramid. The industry and its regulatory and market structures existed to provide customers with an essential service. State and local regulators, directly accountable to customers through the political process, established expectations for that service with respect to safety, price, rate stability, service quality, reliability, environmental attributes, and other features.

This regulation ensured that load serving entities, LSEs, served the public interest. Federal regulation of interstate wholesale and transmission service under the Federal Power Act was interstitial. It was intended to fill the Attleboro gap by providing for regulation of matters beyond the authority of the states to regulate. It was intended to assist the states in carrying out their public interest responsibilities in regulating retail and local distribution service.

State regulation has changed over the years, more in restructured states than in the others. But, the basic responsibilities are unswerving. Even during the throes of restructuring, states maintained responsibility for protecting the public interest.

Most restructured states implemented multi-year rate freezes, designated regulated default suppliers to ensure continued quality of service for those who did not or could not choose competitive suppliers, set expectations for how default suppliers would meet their obligations, adopted customer protection requirements for competitive retailers, and established renewable energy requirements for suppliers.

The LSEs, traditional or competitive, are one step down the pyramid in the traditional industry view. Subject to state regulation and customer pressure, LSEs acquire the portfolios of resources they need to meet their obligations.

LSEs started out largely building and operating their own resources or buying regulated wholesale requirements service from those utilities immediately adjacent to themselves. Over the past twenty-five years, they have increasingly looked to bilateral and organized wholesale markets and to distributed or customer-side resources, to meet their obligations to serve their customers.

That broader range of resources has permitted LSEs to do a better job of optimizing across the portfolio of generation, transmission, distribution, and behind-the-meter resources to meet the wide range of goals established by state regulators and customers.

This history, then, helps to define the original role of the wholesale markets, which sit one level further down in the traditional pyramid. Open and non-discriminatory wholesale transmission services and competitive bilateral and organized wholesale energy markets enable LSEs to serve retail customers better than they could entirely on their own.

This is why LSEs such as municipal utilities and electric cooperatives were among the strongest proponents for open access wholesale transmission service in proceedings at the Commission in the late 1980s and early 1990s.

See Figure One.

Commission Order Numbers 888 and 889 revolutionized the industry by giving LSEs access to a new world of wholesale resources. Open access and wholesale competition opened the door for LSEs to obtain power from entities other than their immediate neighbor.

They could buy economic energy from more distant utilities and enter into bilateral power purchase agreements with merchant generators where those generators could serve them more reliably or at lower cost. Those agreements could help them hedge risk, meet state renewable energy requirements, or otherwise satisfy their obligations to customers and regulators.

In the regions where they formed, ISOs and RTOs offered LSEs new advantages. Independent operation of the transmission system was a further protection against undue discrimination in wholesale transmission service.

RTOs provided regional transmission service at a single rate, eliminating uneconomic pancaked transmission charges. RTOs had responsibility for ensuring short-term grid reliability and for managing congestion. Centralized economic dispatch of generation further brought down the cost of energy.

Somewhere along the way, however, the Commission and some of the RTOs lost their way. They inverted the pyramid. They elevated the RTOs and their relentless pursuit of the lowest marginal cost resources to the top, and deposed retail customers, the state and local regulators that represent them, and the LSEs that serve them.

Each of the conflicts listed in the opening paragraph arises from that inversion. Rather than the wholesale markets serving the needs of LSEs, so they can serve retail customers in accordance with state and local regulation, the LSEs, state and local regulators, and retail customers are being asked to play second fiddle to the RTO markets.

Let's start with the nearly continuous litigation in the three eastern RTOs over the past ten years, owing to conflicts between organized wholesale markets on one side and state policy and self-supply on the other. Before the pyramid inverted, there was no conflict.

By ensuring open access to the transmission system and economic dispatch, the RTOs and their organized markets facilitated LSEs' efforts to acquire the resources they needed to meet customer needs as defined by state and local regulators.

The RTOs' residual capacity markets permitted LSEs to build resources, contract for them in the bilateral market, or purchase power through the organized capacity markets. And, the prices in those markets reflected the free interaction between supply and demand across all the markets.

Conflict didn't arise until the Commission and the RTOs concluded: organized capacity market prices were too low to attract merchant generators relying solely on the organized markets for revenue; merchant generators chosen by organized markets were a "better" resource option than what the states and LSEs chose to meet their needs through bilateral contracts because they were lower cost as the RTOs evaluated cost; and RTOs' pursuit of lower cost was more important than the other values states and LSEs sought to pursue, such as long-term reliability, risk hedging, and environmental performance.

In short, conflict didn't arise until the Commission and RTOs concluded that price formation in the organized wholesale markets should take precedence over the service retail customers sought through the political process.

Until that point there was no need to alter the original residual capacity market designs. There was no need to litigate over the relative merits of minimum offer price rules and divided capacity auctions.

Conflict didn't arise until the pyramid was inverted.

The resilience issue - that the Secretary of Energy has prompted the industry to address - arises from the same inversion. States and LSEs understand the importance of resilience. States and LSEs have not pursued fuel and resource diversity for their own sake. They've done so because they understand that placing all your eggs in one basket has both reliability and economic risks.

The system needs to be planned to ensure that it can survive and quickly recover from shocks whether those shocks are driven by weather, fuel availability, changes in fuel prices, or the loss of major system elements.

That works when state and local regulators and LSEs are permitted to make those plans. And when they are permitted to support those resources (and only those resources) they believe best balance the goals - including resilience - that are included in the "public interest."

That approach does not work when preempted by an organized wholesale market design that pursues the lowest marginal cost resources regardless of the values those resources may offer customers or the system.

We can also see this same inversion in the Commission's recent discussions of the role of state and local regulators, or "relevant electric retail regulatory authorities." In Order Numbers 719 and 745, the Commission established rules for the participation and compensation of demand response in the RTOs' organized markets.

In so doing, the Commission was sensitive to the impact that its orders could have on the retail services regulated by the relevant authorities. To permit them to protect the public interest, the Commission required RTOs to respect relevant authorities' decisions as to whether third-party aggregators would be permitted to bid demand response into the RTO markets.

In upholding the Commission's authority to establish compensation rules for demand response in organized wholesale markets (and in concluding that the Commission was not regulating retail sales), the Supreme Court explicitly relied in FERC v. EPSA on the Commission's decision to give the final word to the relevant authorities.

Unfortunately, the Commission backed away from that position in its initial and rehearing orders in the Advanced Energy Economy case, involving the participation of energy efficiency resources in PJM's capacity market.

In those orders, the Commission determined that it had no obligation to grant relevant authorities the same accommodation with respect to the aggregation of energy efficiency resources. The Commission said its obligation to ensure effective wholesale markets trumped local concerns.

The Commission held that it has authority to decide if and when relevant authorities should be accommodated. It said the Supreme Court's reliance on their rights in the EPSA case was superfluous dicta. This same issue is also at play on rehearing of the Commission's order on participation of electric storage resources in organized wholesale markets.

The Commission's order in the Advanced Energy Economy case makes sense only if the RTO markets truly are at the top of the pyramid. If, however, the retail customer is at the top of the pyramid, then RTO markets should be designed to facilitate LSEs' ability to serve those retail customers. And the relevant authority should be the entity deciding whether those customers are best served by LSE or third-party aggregation of behind-the-meter resources.

That decision should be easy. Local authority is essential given the critical role those resources can play in: local distribution safety, reliability, power quality, and costs; the role they can play in an LSE's integrated resource plan; and the degree to which states have managed the treatment of those resources to protect customers and the public interest.

If we are to resolve these conflicts in a consistent fashion, the Commission must recognize that the centralized wholesale electric markets are a supporting actor in the electric utility industry. They are important to the plot. But, they are not the author, producer, director, and leading actor in the play. It is time for the Commission and the RTOs to adopt a culture of service and design centralized wholesale markets that facilitate the local choices and local decisions of retail customers, relevant authorities, and LSEs.

Wholesale customers should be able to acquire the resources they, their regulators, and their customers want at just and reasonable rates. The pursuit of "just and reasonable rates" evaluated in a vacuum should no longer serve as an unlimited justification for jurisdictional expansion or preemption of wholesale customers' purchasing preferences, state policy decisions, and the protection of retail customers.