The Brattle Group

Specializing in the markets, policies, regulation, and transformation of the electricity industry, Peter Fox-Penner advises U.S. energy companies, grid operators, and government agencies. He has testified before federal and state courts, FERC, arbitrations, and public service commissions. He has served as a regulatory and strategic advisor to boards and executives at utilities and energy companies across the country.

Roger Kranenburg was formerly VP of Strategy & Policy with Eversource, responsible for developing, communicating, and overseeing Eversource’s long-term energy and growth strategy and policies, and leading transportation electrification. He also led federal affairs on funding and legislative and regulatory matters. Prior to Eversource, he was with IHS Markit advising electric utilities, power sector owners, and suppliers in North America, Europe, and globally.

Electricity demand is growing rapidly in the developed world, driving utility capital investments, but also presenting challenges for all industry stakeholders. Clean capital efficiency, which is leveraging technology to drive higher efficiency and utilization of existing and new system assets, is a valuable part of the picture and an important way to help alleviate rate pressure.

Even before electric demand began its recent upturn, the U.S. electric system had its challenges. Much of the industry’s infrastructure was aging and required investment. Increases in severe weather events began to necessitate larger investments in resilience, and reducing the industry’s emissions became a clear priority voiced by customers. We also began to bump up against transmission constraints, unlike previous periods when the system could easily accommodate new generation.

Over the last few years, things have started to change. Electrification, reshoring of manufacturing, and further cloud-based, digitized processes pulled electric demand up from a ten-year growth slump.

Apart from the utilities who were deeply affected by wildfires and other major events, rates rose at close to the rate of inflation, and utilities performed reasonably well, including a thirty-nine percent decrease (since 2005) in carbon emissions — despite higher sales. However, higher inflation and interest rates then started taking a toll, sending several industry health indicators in the wrong direction.

Against this backdrop, the sudden onset of unprecedented power demands from data centers have driven the industry’s multiple challenges into overload. By 2030, data centers will add twenty-five to seventy gigawatts or more demand, depending on whose forecast you believe.

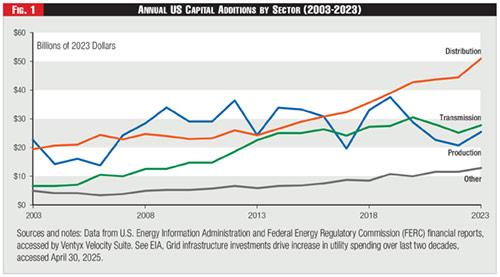

Figure 1 - Annual US Capital Additions by Sector (2003-2023)

Figure 1 - Annual US Capital Additions by Sector (2003-2023)

With electrical equipment costs rising much faster than inflation, a need to meet demand quickly with investments, sometimes years before they are fully utilized, and the ongoing imperatives to reduce emissions, the industry is on a three-way collision course among affordability, climate responsibility, and the sheer ability to timely meet demand.

Hallmarks of the New Era

Driven primarily by technology changes and market forces, energy efficiency (along with demand response and other automation) has been one of our largest resources for many decades. Even with the ever-increasing digitization and electrification of our economy, electricity use per dollar of GDP has dropped by an impressive sixty percent since the year 2000, according to federal government analysis.

Nevertheless, the industry has mainly met most of the recent visible demand increase with increased supply. Since the bump in generation efficiency triggered by combined cycles rolled in thirty years ago, not much has changed in overall system efficiency.

Rates have remained stable mainly because natural gas prices have declined and the cost of solar and wind power has declined very deeply and very quickly. These declines in generation costs have offset the increased cost of maintaining, replacing, and expanding transmission and distribution. It is striking to see that industry generation capital outlays are now the smallest part of electric capital additions and distribution outlays are the largest — almost three times as large.

Peter Fox-Penner: Clean capital efficiency, which is leveraging technology to drive higher efficiency and utilization of existing and new system assets, is a valuable part of the picture and an important way to help alleviate rate pressure.

Peter Fox-Penner: Clean capital efficiency, which is leveraging technology to drive higher efficiency and utilization of existing and new system assets, is a valuable part of the picture and an important way to help alleviate rate pressure.

See Figure 1.

However, there are many signs that this helpful pattern of cost shifts has run out of rope. Driven by sustained higher power demands, the underlying commodities needed for electric power, from copper and steel to rare earth metals, are on a long-term upward cost trend. Similarly, the costs of manufacturing gas turbines and other electrical equipment is increasing, and overstretched supply chains are causing long delivery delays and premium pricing.

Solar, wind, and batteries are going to continue to decline in costs, however, recent policy shifts will create headwinds. Meanwhile, the price of natural gas is unlikely to decline much further. On the positive side, geothermal and nuclear may have cost decline learning curves, but these are very unlikely to kick in at scale in the next decade.

We cannot rely solely on cheaper supply to offset the combination of the rising costs of generation equipment, the fast-rising costs of building out and replacing transmission and distribution, and the short- (if not long-) term imbalance between supply and demand.

Roger Kranenburg: To ensure continued success in the future, we believe investments in transmission and distribution efficiency and flexibility will have to be paired with changes in investment planning, engineering, and operating procedures.

Roger Kranenburg: To ensure continued success in the future, we believe investments in transmission and distribution efficiency and flexibility will have to be paired with changes in investment planning, engineering, and operating procedures.

The numerator effect — all the sources of electric cost increases — are in most cases likely to outstrip the effect of spreading costs over higher sales — the denominator effect. Of course, this puts pressure on customer rates and on utility profits. It is the mirror image of most of the twentieth century when economies of scale lowered unit costs and allowed rates to drop while profits remained stable.

The Future is Bright and Efficient

We will certainly need a variety of clean supply and demand resources to meet demand, reduce emissions, and maintain affordability. Ignoring any of these would be harmful. Rather than only adding more expensive supply-side capital to the balance sheet, there has never been a time in the industry’s history when it made more sense to work hard to increase the underlying system efficiency to get more energy services out of the capital that we have and will add. But how, exactly, can we do this?

In past eras, we generally looked to the generation sector for either technical improvements or cost reductions. There didn’t seem to be many technologies available that could significantly change the efficiency of the transmission and distribution system or make the entire system more interactive between supply and demand.

This era is different. Technology has advanced to the point where control of the transmission and distribution grid along with material science breakthroughs is having dramatic impact in increasing system throughput.

New Grid-Enhancing Technologies (GETs) in the form of advanced conductors, power system and topology controls, dynamic line monitoring and rating technology, and distribution system monitoring and control systems can greatly increase energy throughput on T&D systems with comparatively small capital costs.

Storage is changing the entire character of the system at both the grid edge and in the bulk system. Just as importantly, the current generation of customers isn’t fazed by the idea of algorithmic control of the things they own and use; instead, they now expect it. Last but not least, the shift in real electricity prices and improved technologies are creating an expanded field for cost effective energy efficiency programs.

Clean Capital Efficiency

Under the present set of challenges these changes to our industry represent an extraordinary opportunity to provide more energy services with less added utility capital. If more services are delivered with less costs, the denominator counterbalances the numerator effect and unit rates could be pushed down.

To give this strategy a name, we call it clean capital efficiency. The idea is simple: use the next generation of AI-enhanced technologies to make the overall system more flexible, responsive, and efficient, rather than larger.

This is obviously a good idea from the standpoint of affordability. However, modernizing transmission and distribution will also continue to make the system cleaner by managing demand growth and integrating more renewables upstream and downstream.

It will help with the evolution of the electric system architecture while supporting reliability, resiliency, and cybersecurity. It is also one of the fastest ways to add effective capacity to the system, as it bypasses many supply chain and transmission bottlenecks.

Electric utilities do a remarkable job running a huge, complex, and essential system. To ensure continued success in the future, we believe investments in transmission and distribution efficiency and flexibility will have to be paired with changes in investment planning, engineering, and operating procedures.

This will be no small lift, but it is a challenge that utilities could meet head-on. There will be plenty of new supply infrastructure to finance and build. As we move forward, effectively harnessing current and future generations of technology to build a smarter, more efficient electric system is essential to our well-being, security, and economy.

Acknowledgement: This article is based in large part on a white paper, “Affordability, Rates, and Clean Capital Efficiency: A Path for the Power Industry’s Turbulent Next Decade,” coauthored by Fox-Penner, Ryan Hledik, Shannon Paulson, and Xander Bartone. See the paper on the PUF website for additional background and acknowledgements.