No One-Size-Fits-All Solution

Molly Podolefsky is a Ph.D. economist and leader in the energy and sustainability industry with experience spanning decarbonization, the utilities and energy sector, finance and investment and business management. As a Managing Director with Clarum Advisors, she leverages her knowledge and experience working with utilities, startups, corporations and funds in the energy transition space.

Noah Podolefsky is a Ph.D. physicist, innovator and thought leader with over fifteen years in the battery energy storage systems (BESS) space. As a Senior Advisor with Clarum Advisors, Noah leverages his extensive knowledge of the BESS industry and business strategy assisting funds with investment due diligence, large corporations with BESS innovation, and energy storage startups with growth and commercialization strategy.

The landscape for long duration energy storage (LDES) is complex and rapidly evolving. Pumped hydro storage (PHS), the mainstay of LDES over the last century, requires specific geographic features that have largely been exhausted in many regions. At the same time, the rapid growth of variable renewable energy (VRE) generation through wind and solar requires ever larger tranches of energy storage to firm capacity, ensuring grid reliability and resilience.

The resulting market need has led to an explosion of creativity in the LDES space, with novel technologies, from R&D to early-stage commercially viable solutions rushing to fill the gap.

The future of this market depends on regulators, buyers, and investors making choices today that will accelerate the market toward an efficient future state, yet the market is complex and rapidly evolving. To untangle this dimensionality, we present a structured framework for analyzing the LDES market today, at the start of 2026.

LDES Technologies and Key Characteristics

Four categories containing over fifty unique solution types comprise the LDES market today:

Mechanical — Pumped hydro, compressed air, liquid air, cryogenic, gravity;

Molly Podolefsky: Energy providers with more aggressive decarbonization goals and requirements will face higher variable renewable energy penetration in the near term, accelerating the need for LDES.

Molly Podolefsky: Energy providers with more aggressive decarbonization goals and requirements will face higher variable renewable energy penetration in the near term, accelerating the need for LDES.

Electrochemical — Flow, metal-air, and lithium-ion batteries;

Thermal — Heat-based and cold-based thermal to electric storage; and

Chemical — Hydrogen storage, ammonia storage, power-to-synthetic fuels.

Thirteen key characteristics determine the applicability of LDES solutions to market needs:

Noah Podolefsky: This framework reveals that while the global market may favor certain technologies, there is no one-size-fits-all solution, and therefore a single technology will not emerge as the sole winner.

Noah Podolefsky: This framework reveals that while the global market may favor certain technologies, there is no one-size-fits-all solution, and therefore a single technology will not emerge as the sole winner.

Cost — CapEx and levelized cost of storage (LCOS) are both considerations, while decreasing cost by duration and very low marginal dollars per kilowatt hour are often keys for success;

Cycling — Frequency of charge/discharge cycles to optimize degradation rate and lifetime energy throughput;

Duration — Intra-day (three to twelve hours), day-long (twelve to twenty-four hours), multi-day (twenty-four to one hundred hours), and seasonal (weeks to months) serve overlapping and distinct needs;

Efficiency — Low (less than forty percent), medium (forty to eighty percent), high (greater than eighty percent);

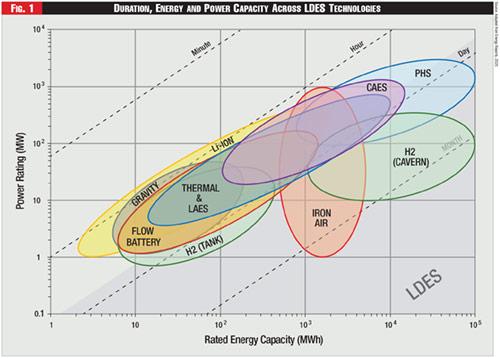

Figure 1 - Duration, Energy and Power Capacity Across LDES Technologies

Figure 1 - Duration, Energy and Power Capacity Across LDES Technologies

Energy Capacity — In megawatt hours, governs the total energy the system can provide per cycle;

Geographic Constraints — Environment, elevation, water reservoirs, caverns, and physical footprint requirements can constrain feasible deployment of some technologies;

Input Constraints — Reliance on scarce metals and minerals negatively impacts market potential;

Lifetime — The number of charge/discharge cycles (cycle life) and maximum age (calendar life), impacts LCOS;

Technology Readiness Level — Maturity of technology used for procurement decision making, impacting near-term uptake and bankability;

Commercial Readiness Index — Readiness for adoption, maturity of manufacturing, supply chain, and standardization;

Power Capacity — Maximum sustained discharge rate in megawatts determines ability to meet peak load demands;

Safety — Risks associated with thermal runaway, fire propagation, toxic gases, and other considerations negatively impact adoption and bankability; and

Scalability — System modularity and decoupling the scaling of energy from power improve suitability for many applications.

Framework for Understanding the LDES Market

In our view, a purely technology-based framework fails to bring the market into focus for decision makers. We propose an alternative framework for understanding the LDES market, driven by the needs of buyers. Energy providers and data centers are the two largest markets for LDES.

We exclude other C&I customers due to the small, nascent market, and government agencies which are relevant only in the near-term as they seek to buy down cost-curves, advancing technologies relevant to key customer groups in the future.

Energy Provider Needs and Priorities: Utilities and other load-serving entities (LSE), today's leading buyers of LDES, require a resource they can count on during the worst hours and days of the year, when renewables intermittency, peak demand, grid constraints, and weather collide.

Those energy providers with more aggressive decarbonization goals and requirements will face higher VRE penetration in the near term, accelerating the need for LDES.

The highest priorities for these buyers are:

Resource adequacy — Sufficient power capacity (megawatts) at all hours of the year to meet peak demand, capacity obligations and regulatory requirements in the face of growing demand, large load connections, unpredictable weather conditions, and increasing reliance on VRE; and

Reliability and resilience — Clean, firm, dispatchable power available 24/7, to supplant fossil generation and peaker plants, while filling the gaps left by intermittent VRE and providing backup power for outages and natural disasters.

The most important characteristics for these buyers include:

Asset Life — Long lifetime, twenty to forty plus years;

Cost — Low-cost technologies address energy affordability and enable cost recovery;

Duration — Eight to twelve hours in the near-term, with multi-day needs increasing with VRE;

Power Capacity — Twenty-five to three hundred-plus megawatt blocks;

Safety — Low-risk, safe, proven technologies regulators will approve; and

Siting — Flexibility to site at transmission nodes, substations, and load pockets.

Data Center Needs and Priorities

Data centers require clean, reliable energy 24/7, have very low tolerance for power supply disruptions, and face scrutiny from the public and regulators over carbon emissions and grid and energy affordability impacts. Customers in this rapidly expanding market are unlikely to purchase LDES outright, preferring procurement through long-term contracts or partnerships with utilities and storage providers.

The highest priorities for these buyers are:

Clean Firm Capacity — Clean, dispatchable capacity and backup power to meet aggressive decarbonization goals, including 24/7 carbon-free energy use, while meeting the reliability needs of users with zero tolerance for downtime; and

Grid Congestion Relief — Peak load reduction, by charging LDES off-peak and deploying on-peak, facilitates interconnection on congested grids around data center clusters, where the LSE could not otherwise accommodate new large loads without additional infrastructure buildout.

The most important characteristics for these buyers include:

Asset Life — Aligned with twenty- to thirty-plus year data center campus lifetime;

Duration — Eight to seventy-two-plus hours, shorter duration for grid congestion relief, longer duration for clean firm capacity and backup power;

Power Capacity — Five to one hundred fifty megawatts of modular capacity, scaling with facility size;

Safety — Proven safe, low-risk technologies to suit dense data center complexes close to communities and occupied buildings;

Scalability — Preference for modular LDES solutions given the modular scaling of data centers; and

Siting — Flexibility needed in siting to match data center needs based on availability of fiber optic lines, affordable land and water, and beneficial tax policies.

As shown in Figure 1, duration, power capacity, and energy capacity, are important determinants of the suitability of LDES technologies to different use cases. The shaded area denotes durations greater than eight hours, indicating technologies applicable to LDES.

See Figure 1.

Best Fit LDES Technologies

Energy providers' and hyperscalers' needs, though slightly different, result in the same set of best-fit LDES technologies given the increasing importance of VRE to both. Based on the highest priority needs and characteristics described above, and prioritizing technologies that have achieved a reasonable level of technical and commercial readiness, the following technologies stand out:

Carbon dioxide batteries — Ideal for daily firming for utilities and in support of 24/7 CFE for data centers, mechanical carbon dioxide batteries exhibit relatively high efficiency (less than seventy-five percent round-trip), very long lifetime (thirty-plus years) and zero reliance on critical minerals — though their large footprint can hamper flexible siting in dense urban environments; medium technology readiness level (TRL), relatively new with prototype demonstration projects in operation; low commercial readiness index (CRI), commercial projects currently in development;

Flow batteries — Ideal workhorse for high cycling intra-day needs, electrochemical flow batteries such as vanadium redox provide very long asset life (thirty to fifty-plus years), are ideal for daily deep cycling, and offer modular scalability by adding tank volume, though mineral price volatility could constrain adoption of vanadium systems; some high TRL, mature and fully demonstrated (vanadium) with lower, lab-scale (organic); low CRI, continued challenges with cost, efficiency, and supply chain;

Iron-air — Ideal for multi-day energy backup for utilities and data centers, iron-air batteries provide very long duration power (fifty to one hundred-plus hours), at extremely low cost — the mature target installed system cost is twenty dollars per kilowatt-hour as compared with upward of eighty dollars per kilowatt-hour for Li-ion battery energy storage systems (BESS); degradation is significantly lower than Li-ion batteries given low cycling; medium TRL, relatively new with prototype demonstration projects in operation; low CRI, commercial projects currently in development;

Lithium ion (Li-ion) — As a bridge technology, Li-ion systems play a dual role providing short duration (two to four hours) plus mid-range (up to twelve hours), with relatively low costs driven by the electric vehicle industry, and recognition by investors and regulators as a mature technology; thermal runaway and fire safety remain critical concerns; high TRL, fully mature and proven; high CRI, fully commercialized with international standards, known manufacturing methods, and supply chains.

Recent Implementations and Looking Ahead

Examples of recent LDES implementations and demonstrations include:

Ark Energy — 275 megawatts and 2,200 megawatt-hours, Ark Energy's Li-ion installation under development for the Richmond Valley Solar Farm in New South Wales, Australia, will be the world's largest eight-hour Li-ion implementation, and is expected to be operational by 2028.

Energy Dome — Google announced a global commercial partnership with carbon dioxide battery LDES producer Energy Dome in 2025 in support of its 24/7 CFE goals.

Form Energy — One and a half megawatt iron-air pilot with Great River Energy in 2025, delivering peak power continuously for a hundred hours and scheduled for operation in 2025.

XL Batteries — Prometheus Hyperscale contracted with XL Batteries to implement a three hundred thirty-three kilowatt organic flow battery pilot serving one of its data center locations in 2027, with a twelve and a half megawatt commercial-scale implementation to follow in 2028.

This framework reveals that while the global market may favor certain technologies, there is no one-size-fits-all solution, and therefore a single technology will not emerge as the sole winner. Though iron-air, carbon dioxide, and flow batteries in tandem with Li-ion appear best suited to serve the needs of most utilities and hyperscalers, depending on geographic constraints and needs of buyers, hydrogen, gravity, thermal, and other emerging technologies may play important roles in the future development of LDES.