Three ‘power plays’ for utilities seeking growth.

As managing director for utilities strategy at Accenture, Greg Bolino works with clients to use digital capabilities to transform the business, adopt new business models, and drive value from smart grid investments.

The business model of the traditional utility company is breaking down - but in different ways for individual utilities. Ironically, however, this may be a good thing for the industry, as it may help to point the way forward. Otherwise, if utilities should try to adhere to their current ways of doing things, they would likely find it difficult to meet objectives for growth.

Utilities today face a wide range of factors that stand in the way of continued growth, stemming mostly from new technologies. In our own research last year, we found that 61 percent of utility executives globally believe distributed generation will have a negative effect on revenues, up from 43 percent the previous year. Even more startling, 60 percent of those surveyed said they believe the much-dreaded industry "death spiral" of significant demand disruption will occur within the next 10 years.

Major Threats

We have identified a handful of major threats eroding the typical utility business model:

Reductions in Demand. We see a 15-percent potential reduction in demand by 2025, stemming from rapidly evolving energy technologies.

Competition from New Players. The industry resembles an evolving ecosystem, with new business models and partnering opportunities arising daily. For example, 90 percent of executives believe competition will increase for beyond the meter services in the next five years.

Figure 1 - Business Models Face Threats

Figure 1 - Business Models Face Threats

Changing Customer Expectations. Customers want a simple, engaging experience. And 57 percent of consumers we surveyed said they were likely to purchase connected home products and services in the next five years.

Changing Policy Goals. Regulators today want to see a greater focus on efficiency, utilization, optimization, and conservation. Achieving these goals will require a fundamental shift in the role of utilities.

Rising Costs. In North America, the customer service costs of top-quartile utilities now run 89 percent higher than in 2005. And pressure is rising on operations costs, due primarily to the complexity of the network (as shown through analysis by Accenture and Capital IQ).

Clearly, utility companies have reached a critical juncture. Their foundational mandate is the "obligation to serve," which historically drove one of the most successful investment programs in modern society. Under this regime, the returns earned on regulated assets encouraged utilities to build capacity to meet peak demand. But in a world of distributed generation, energy efficiency, and alternative energy sources, this model is no longer optimal. It can't be sustained.

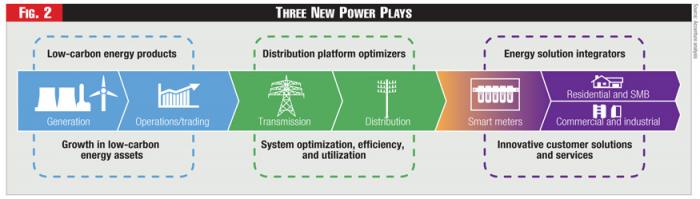

Figure 2 - Three New Power Plays

Figure 2 - Three New Power Plays

In this new energy world, business models should focus not just on transporting and delivering peak energy, but on optimizing energy sources, distribution systems, and demand - all while enabling utilities and other companies to meet the evolving needs of their customers.

Right now, utilities need to make strategic choices to redesign the scope of their services and to shape the role they will play in this evolving market. We see three possible paths for utilities to take. These "power plays" offer the potential to re-define the value chain and put utilities on a new path of growth and profitability. No single model will work for all utilities, and these options are not mutually exclusive. Utilities should consider the merits of each as they make business portfolio decisions.

Possible Answers

Consider these three possible "power plays" for remaking the utility business model:

- Low-Carbon Energy Producer

- Distribution Platform Optimizer

- Energy Solutions Integrator

The first of these three suggested new models - that of a low-carbon energy producer - is already accelerating the transition to a more climate-friendly energy supply market in both regulated and deregulated asset portfolios. Traditional power generators have seen their portfolios change considerably because of changing economics. Successful producers would continue to make strategic portfolio choices that shift the mix and capture incentives design to foster migration to lower-carbon supplies. These choices will require strong balance sheets and access to financing.

Over time, players choosing this model will likely come to resemble mining or commodity chemicals companies. They will likely establish global operations and shared-support services across a diverse array of assets - both to reduce fixed costs and to improve capital project performance. In addition, they would require leading capabilities in areas such as asset management, continuous process improvement, and capital project management. Such companies will transform themselves with digital capabilities like real-time analytics and digitally-enabled workforces.

The second model, that of distribution platform optimizer, most clearly illustrates the industry's shift from an "obligation to serve" to a "commitment to optimize." This shift will entail a greater focus on utilization, optimization, efficiency, and conservation. In this model, the distribution utility serves as an energy clearinghouse. It addresses consumer demand by choosing the most appropriate sources. The platform optimizer adjusts operating practices to help meet demand most efficiently, such as running the grid based on changing loads, establishing tariffs tied to grid economics and stress points, and creating new interconnections to optimize distributed resources.

Our distribution platform optimizer will play another important role as well - to foster new interconnection standards to help third parties gain access to markets and also to allow demand management practices to become more dynamic.

For example, voltage inverters used in solar and battery installations would operate with industry-defined operating standards, including dynamic integration and signals from the distribution system. And technology standards would ensure interoperability - for example, to ensure that vehicle connection points can be modulated or utilized, if allowed, as storage. More creative interconnection agreements also would make it easier for to integrate public-purpose assets like community solar resources or enterprise microgrids.

To transition to this model, traditional utility distribution companies would have to collaborate with regulators and other stakeholders to develop a performance-based model for distribution. This model would have to reward utilities that succeed in optimizing the system and achieving superior results along various key outcome metrics, such as renewable integration, system utilization, demand smoothing, and total system losses. Utilities also will need to adopt "intelligent" network capabilities, including real-time network controls, distribution automation, and device-level intelligence. And the distribution companies would need to transform themselves with digital capabilities that enable asset analytics, storage integration, and digital field work.

Some utilities already are pursuing elements of this model. For example, utility pilot projects are demonstrating the use of digital devices and battery storage to integrate renewables on the network, or are using storage and network control devices to offset investments in traditional assets. These efforts mark the front edge of the transformation of the distribution company.

Now we move to our third suggested model, that of the energy solutions integrator.

Customers want answers to help them manage energy in their homes and businesses. Our own research indicates that nearly three-quarters would turn to their energy provider for solar products, for monitoring and control solutions, and for support for electric vehicles.

Energy solution integrators would play in this rapidly evolving market to provide customers with choices. They would provide services that help customers not only to optimize energy production and use, but also to provide greater control, convenience, and comfort. For example, utilities might install, finance, run, and maintain energy assets such as distributed generation and electric vehicle charging stations. Other service categories include smart HVAC and appliances, connected home devices, energy management, and efficiency services. As technologies and customer behaviors evolve, new service opportunities are likely to emerge.

The key differentiator for players adopting this model would start and end with customer convenience - a clear and recognized brand, a simple experience, and flawless execution. Players in these services today know that digital models can prove especially effective and economical - for analytics, for real-time decision engines, and for marketing and service fulfillment.

Whether the retail commodity is regulated or liberalized, the solutions market will become vibrant and competitive, as illustrated by the players already offering services in these categories. Companies that prove successful with this third new business model will be those that establish new strategic partnerships, along with strong capabilities in vendor and contract management. Nevertheless, few players to date have been able to combine digital devices and services with the ability to take advantage of the economics of the energy system. Therein lies a unique advantage for traditional utilities.

Making It Work

To be successful in these new models, utilities should be preparing now. And here's how.

First, choose a strategy that makes sense with your current portfolio. That will require a shared vision among your company's leaders concerning the impact of changes and a blueprint for the future. Now is the time to ask hard questions about future growth - and about the prospects for growth under the current business model.

Second, as you define a new vision, take care to invest in building those capabilities that will protect earnings today but also deliver results for the new chosen business model. Such options might include investments in grid automation, regulatory and tariff reform, and new customer interaction and service models.

Third, remember that digital capabilities adopted today can transform the performance of the current utility business. That includes digital capabilities in managing assets, field work, the operation of the grid, and in serving customers. Digital capabilities already are lowering barriers to entry for potential competitors and showing customers how new models can work. Going digital will help your utility not only to achieve current business objectives, but also to succeed in your emerging business model.

A carefully designed roadmap can offer advantages. For example, a digital roadmap can help reduce costs - both for direct customer service as well as operations and maintenance. It can help you reduce the cost to fulfill and manage energy programs such as demand response and efficiency initiatives. And it can help you prepare to reduce the impact of integrating distributed generation.

Threats to the utility business model mean that it's time to make choices about future growth. The risk of waiting to reform is growing every day. Yes, you will need to protect your current cash flows while investing in new capabilities. Yet these new capabilities will take time to mature. All this will require patience and flexibility. But the time to choose - and to act - is now.