The Clean Power Plan's largest obstacle is how its cost is distributed disproportionately among the states.

David Bellman is Founder and Principal for All Energy Consulting. Contact him at dkb@allenergyconsulting.com.

The largest obstacle looming within the Clean Power Plan proposed in June by the U.S. Environmental Protection Agency (EPA) will not be the overall cost of the program, but how that cost is distributed disproportionately among the states. As a nation, the overall impact may not seem large for many. But in some states, it will severely alter the current economic surroundings. This plan becomes a test of the federal power versus states' rights. Using EPA's supplied analysis and our advanced highly sophisticated power market models, we will demonstrate that the cost of the plan is more onerous in some states than others.

On June 2, 2014, the U.S. EPA proposed rules to reduce CO2 emissions from existing power plants through Section 111(d) of the Clean Air Act (CAA). The rule is also commonly called the "Clean Power Plan." There are some key nuances that should be immediately understood.

The proposed rule covers existing power plants only - meaning that new units built would not be impacted by this ruling. The new plants are subject to 111(d), which essentially supports building natural gas combined-cycle plants. Given that EPA is targeting only existing units, it is proposing a state-by-state rate target, or pounds of CO2 per MWh.

Each state is required to submit a plan that would achieve that state's EPA-targeted emission rate. This emission rate will represent the amount of emissions divided by the energy produced. The unit EPA uses is pounds (lb) per megawatt-hour (MWh). To calculate a simple state CO2 emission rate, add the total CO2 emissions from all existing units and divide by the energy produced by the unit. EPA has added complexity in determining the emission rate, as it is allowing the generation of zero-carbon sources to be part of the denominator in calculating the rate as shown in Figure 1.

In past programs, covering both acid rain (SOx) and nitrogen oxide (NOx), EPA targeted a fixed amount of emissions, not a rate-based target. By contrast, the rate-based approach in the Clean Power Plan will enable the state not necessarily to eliminate CO2 emissions altogether, but it will force a transition to lower emitting CO2 plants. That difference reflects the comparative lack of cost-effective emission control technologies for CO2, versus SOx and NOx. CO2 emission control technology is very cost-prohibitive. Therefore, the only means to reduce CO2 is to run generating units that produce fewer CO2 emissions. These two nuances change the approach to typical emissions modeling. Moreover, the EPA should be able to issue and enforce its new ruling without any enabling Congressional action, given that implementation will proceed under the existing Clean Air Act.

EPA’s Assumed Emission Rate Formula

EPA’s Assumed Emission Rate Formula

For the EPA to produce state-by-state targets, it examined four mechanisms to reduce CO2 on state-by-state basis and guesstimated the likely efficacy of each mechanism by state.

These four mechanisms were referred to as building blocks. The four blocks are (1) efficiency improvement at plants, (2) dispatch changes, (3) zero-carbon generation options, and (4) energy efficiency (EE). There were no requirements that any state use all of the building blocks, but given that states can use these blocks to achieve the rate target, it would seem reasonable the cost analysis should represent these blocks. A spreadsheet is available from the EPA presenting the expected impact of each of the building blocks by state.

California vs. West Virginia

The most impactful of the building blocks is the use of zero-carbon generation. Without this building block the CO2 emission rates would be on average greater than 20% from the EPA emission rate targets.

The bulk of the zero-carbon generation sources anticipated by the EPA is the additional renewable generation from wind and solar. The established level of renewable generation used to calculate the rate targets were not generated by economic modeling, but primarily through the use of state mandated renewable goals aggregated into 6 regions. These same state mandates were typically based on political goals rather than economic principles, with several states designing cost caps in the program. The EPA spreadsheet shows 4% annualized growth of renewable generation from 2012 to 2030, which would be reasonable to anticipate given the recent trend. The issue is not the overall growth, but the expectations of how the growth in renewable generation will be apportioned to each state, with some states shouldering a huge economic burden.

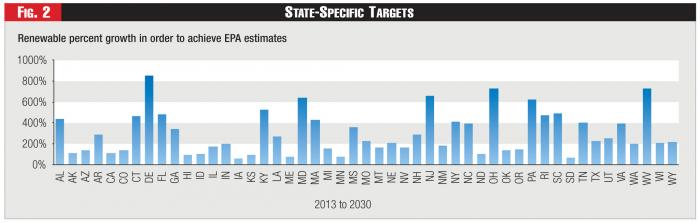

Figure 2 - State-Specific Targets

Figure 2 - State-Specific Targets

Historically, the areas with the greatest renewable development are marked by two key characteristics - high power prices and/or an abundance of renewable generation opportunity. In these areas, the cost hurdle to move to renewable power source was deemed minimal, such as the case in California, compared to states with low power prices, such as Kentucky and West Virginia. These lower-price states will face a much greater cost impact in moving to a more renewable system. Their economies are centered on low power prices. The jump to this higher-cost power will be significant. Figure 2 shows a state-by-state view of how much renewable generation would need to grow, based on the latest 2013 renewable generation levels to hit the EPA guestimates of renewable generation.

West Virginia's growth in renewable is expected to be 732% higher than 2013 renewable generation levels. In West Virginia's case, EPA is asking the state to invest in a more expensive, but cleaner power source. If we assume the cost of renewable generation is $2000/kW with a capacity factor of 30%, then West Virginia's renewable capacity needs total ~3.4 GW, with a total cost of $7 billion dollars.

Using the 2013 retail sales and retail rates supplied from EIA a simple calculation of retail rate impact can be done. Spreading the cost over 20 years based on 2013 retails sales, it would cause a retail rate impact of +14% for West Virginia. (See "Hitting the Target" at the end of this article.)

Conversely, California, using the same assumptions, renewable capacity needs total ~1.7 GW with a total cost of $3.5 billion dollars. With a much larger rate base (California retail sales +8X the amount compared to West Virginia) plus the fact the initial rate is already 84% higher than West Virginia's rate, the overall rate impact for California is negligible (0.5%).

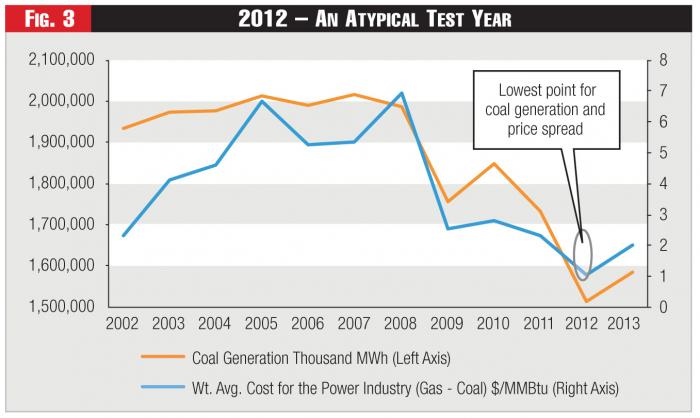

Figure 3 - 2012 – An Atypical Test Year

Figure 3 - 2012 – An Atypical Test Year

Within the most impactful building block, zero-carbon generation, the EPA plan is producing significant state disparity impacts. This is a simple way of viewing the cost difference. The difference in rate impact is likely even greater than stated here as renewable performance in West Virginia (solar insolation and wind speeds) is much less than California. The above calculation assumes the same renewable performance. Of course, growth in renewables would yield fuel savings that would reduce the cost of new investment. However, the fuel savings also will cause greater rate differences as fuel savings in coal states such as West Virginia will be much less than fuel savings in California. The most impactful building block of 111(d) will cause un-even economic strife among states.

Gas versus Coal

The next most impactful building block is the re-dispatching of the system fleet - mainly substituting coal generation with existing underutilized gas-fired generation. This strategy improves CO2 emissions, both in terms of gross tonnage and per-unit emission rates, as gas-fired units emit approximately half the CO2 per MWh (118 lb. of CO2/MMBtu) versus a coal unit (205 lb. of CO2/MMBtu).

Without this building block, the CO2 emission rates would be on average some 18 percent greater than the EPA emission rate targets.

This building block is commonly termed "dispatch." And when dispatch is discussed, one should quickly consider market conditions. A dispatch of power plants is driven largely by load and fuel commodity price relationships. To quantify the volume that can be dispatched differently, EPA increased the 2012 generation of combined-cycle natural gas plants to produce a 70% capacity factor. The increased generation was then subtracted from the coal generation levels.

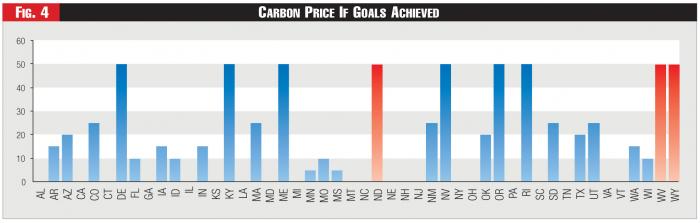

Figure 4 - Carbon Price If Goals Achieved

Figure 4 - Carbon Price If Goals Achieved

EPA is correct about the physical capability of substituting gas generation for coal generation given the surplus capability of gas units. Capacity factor represents the utilization of the plant throughout the year. Thus, a 100% capacity factor represents a plant that runs every single hour of the year at its full capacity. A 50% capacity factor plant represents a plant that would be somewhere between a plant that runs half its capacity every single hour to a plant that runs 100% for half the year and 0% for the other half.

Many plants are built and designed to run 100% for a few hours. For these few hours, power prices are high enough to pay for the limited run time. The existence of many plants that are underutilized is by design. In theory, as EPA has suggested, these units could be run more to replace other generation requiring minimal capital investments from the market. However, to run more requires increased variable cost, as the only reason they are not running more now is there is no price incentive to do so.

Nevertheless, by choosing 2012 as a starting point for its re-dispatch calculation, EPA's assumptions immediately produce a disparity in the ability of certain states to achieve the EPA emission rate targets. Out of all the years one could choose, 2012 is probably the least representative of likely future conditions in terms of commodity price relationships. As shown in Figure 3, the spread between coal and gas prices was less than $0.40/MMBtu during the year. Nowhere in the forecast is this price spread being predicted.

Rather, virtually all industry forecasts expect gas prices to rise faster than coal prices relative to 2012. This fact is important because it makes the cost of generating from gas plants even more expensive than coal plants. Increasing this spread increases the disproportional impact of the cost of the plan as coal-centric states will require greater CO2 cost.

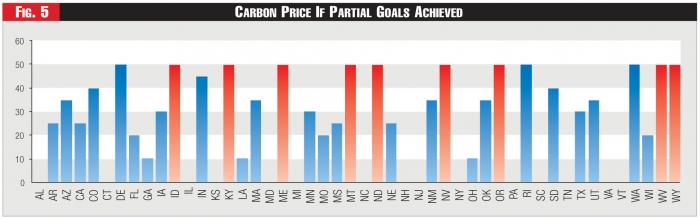

Figure 5 - Carbon Price If Partial Goals Achieved

Figure 5 - Carbon Price If Partial Goals Achieved

In the models being used by EPA, the spread is closer to $3/MMBtu in the long-run forecast. Using this outlier year produces an abnormally low level of coal generation to start their calculation of targeted rate.

States such as Kentucky and West Virginia will appear to have not so great a burden as will a state such as Texas, given the reductions in carbon emissions relative to 2005 can be attributed to less coal generation due to market economics. However, this apparently lesser burden for Kentucky, West Virginia, and the like (for compliance through the re-dispatch block) veers off from reality, as gas- and coal-price spreads will rise and these states will have more to overcome. The economic penalty will be greater in future years as the cost to use gas over coal increases, as the forecasts say it will. The cost of CO2 will need to increase much more in states like West Virginia to compensate the lower cost of coal plants versus gas. Other states with much less coal supply will be minimally impacted. This anomaly will become apparent when we model this through our power models.

To quantify the extent the market would need to change to achieve the building block of re-dispatching more natural gas units, we used our power models. Our models are not policy models. The models we used can make financial decisions in the current market place for both gas and power markets through the product line Power Market Analysis (PMA). The base dispatch model being used is AuroraXMP by EPIS. The entire North American energy market is being modeled. A significant amount of work was needed to produce a model that is applicable to today's market. It is easier to do long-term policy modeling than to try to model the next month's market. There is much more scrutiny and validations needed to support a trading model versus a policy model.

Renewable Energy Prospects

In our calculations we assume that the blocks for renewable generation and energy efficiency are achieved at fixed levels 100% and 60%, as stated by EPA. We use the model to solve for the CO2 price in each state that would produce the needed emissions and generation of existing units to equal the rate targeted by EPA using the above formula discussed. The simulations were all based on the forward curve prices published on June 5th, 2014. It was an iterative approach as we changed state CO2 prices, dispatched the model, recalculated the rate by state, and increased or decreased the CO2 price on an as-needed basis by state - and then repeated the process.

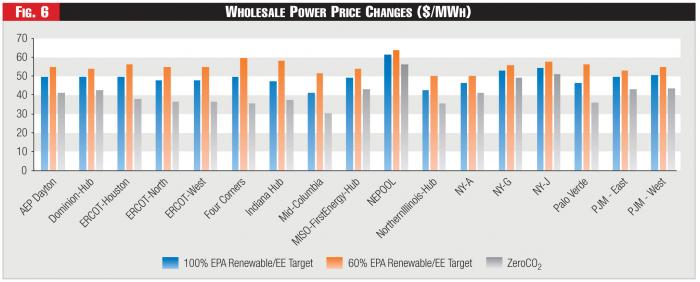

Figure 6 - Wholesale Power Price Changes ($/MWh)

Figure 6 - Wholesale Power Price Changes ($/MWh)

The iterative nature was exacerbated given that electricity knows no state boundary. The flow of electricity is a function of the grid design, which is developed to support a large geographical footprint. Accordingly, as a state changes its CO2 price, it will impact another state's generation. After much iteration, we converged on an acceptable tolerance range and produced the EPA state-by-state targets. There were a few states where the cost of CO2 would have to be greater than $50/ton. Instead of finding the final value, we stopped there as our point is to understand there are some extreme differences by state from this ruling.

Figure 4 represents the case where EPA assumptions for both renewable and energy efficiencies are met. And as Figure 4 shows, North Dakota, West Virginia, and Wyoming would require much higher CO2 prices than $50/ton to achieve the rate targets in their respective areas.

Figure 5 represents the case where EPA assumptions for both renewable and energy efficiency are only met 60%. Compliance at this level for the zero-carbon and EE building blocks would imply that states rely more on switching to gas-fired generation to achieve the EPA's state-specific emissions target rates. In this case, Idaho, Kentucky, Maine, Montana, Nevada, Oregon, West Virginia, and Wyoming exceed the cap of $50/ton to converge to the EPA state target rates.

The impact on the CO2 price will change the individual state generators' performance plus alter the wholesale markets. The impact will directly alter jobs. That's because there is reduced generation that would lead to plant closures. Meantime, increases in wholesale markets could lead to industrial/manufacturing plant closure or re-alignment.

Figure 6 shows the impact on wholesale market prices. In general the power price advantages in certain regions disappear and power prices become more consistent across the country. Optimistically, for the nation as a whole, the plants will stay in the country. But we predict that operations will realign to California, New York, and Texas - states that each have high population counts and easy access to international shipping.

As noted above, the 60% case will likely be real for many states as renewable targets will be hard to meet for some individual state. The hardship may be to the level that the re-dispatching cost may actually be more cost effective. Energy efficiency programs in some states will also see the same fate.

Energy Efficiency

Energy efficiency is the third most impactful block in achieving the EPA targets. Without this building block, the CO2 emission rates would be on average greater than 13% from the EPA emission rate targets. By setting the achieved level of growth in energy efficiency for each state around 10.6% (min 9.3%, max 12.3%) of total state energy demand, we observe an uneven cost structure for many states.

An energy efficiency program is a detailed process. It must focus on how customers are using energy. If customers already use heat pumps to stay warm as their primary form of energy usage, implementing a large light bulb program will achieve only so much, compared to places like California. As weather becomes more temperate, it is easier to modify behavior because human life is not harmed. However, in extreme cold or heat, savings from energy efficiency become limited, as a percentage of total energy consumed. The successful California experience in energy efficiency just cannot be extrapolated one-for-one to other states. Given that EPA's the target energy efficiency level is similar for all states, we predict a significant additional cost for states in less temperate weather.

The final block involves coal power plant efficiency improvement (better heat rates). But it is too small of an impact on which to dwell. Without this building block, the CO2 emission rates would be on average greater than 5% from the EPA emission rate targets.

A Closing Comment

Viewing the EPA Clean Power Plan 111(d) as a national cost makes it easier to accept the reasonableness of the plan. However, as the saying goes, "the devil is in the details." Will the final plan be able to address some of the inequity of the plan to balance the potential economic strife in certain states? Or will the states just roll over - and thereby simply increase the influence of the federal government? This plan is not just addressing the global climate concerns, but it is also reflecting a transition of political power, from the states to the Feds.

- - -

Hitting the Target

Calculating cost and rate impacts.

Over the next 15 years or so, the cost and rate impacts for individual states to achieve the EPA’s state-specific targets for growth in investment in zero-carbon generating resources (read: “renewables”) will vary widely, if we can trust these two fairly simple calculations.

To calculate cost, the two key assumptions are (1) an assumed installed capital cost of $2000/kW for new renewable investment and (2) that new renewables will operate with an overall 30% capacity factor over the course of all 8760 hours in the year.

Further, to calculate the 20-year rate impact in each state for passing that new investment cost along to ratepayers, we need know only the total retail electric sales (kWhs) in that state for the year 2013, plus its average retail electric rate ($/kWh) for the same year, as follows.

Lead image © Can Stock Photo Inc. / tolokonov