As deployments take hold, real-world challenges abound.

Richard Fioravanti is vice president for distributed energy resources at DNV GL. He assists utilities, manufacturers, and policymakers with business plans, financial models, and device testing for advanced storage technologies, microgrids, and other distributed energy applications.

Advanced energy storage is emerging from laboratories and demonstration projects into actual deployment across the power grid. That is evident not only in pockets of activity throughout the United States, but increasingly throughout the world in deployment commitments (in multiple megawatts) by states, island nations, and countries. At the U.S. Department of Energy (DOE) the agency's energy storage database (a voluntary collaborative list of projects) reports 294 advanced energy storage projects totaling 546 MW already operational the U.S., and a total of 611 projects (1.163 GW) operational worldwide. The industry has come a long way in just a few years.

Nevertheless, when a technology enters the deployment phase, the rules change. In deployment, those demonstrating the technology are no longer just researchers but third-party developers with skin in the game - looking both to operate the technology and operate at a profit. The money propelling deployment will be looking not just to demonstrate, but to earn a return on investment. This fact introduces new challenges and information requirements that may not be readily available to the industry. How do you assess and estimate the cost of operating a system over long periods of time? What is the overhaul and maintenance impact of a system that needs to maintain a rated capacity over a 10-15 year period? Tools are available to help developers understand these costs with confidence, but the industry also needs to realize that despite a terrific success in getting the technology out of the lab, there is still work to be done and support needed to get the technology onto the grid - and to operate there in an effective manner for long periods of time.

A Shift in Thinking

Traditionally, storage devices were categorized either as "power" (short duration) or "energy" (long duration). However, when stakeholders started looking carefully at storage as an application and applying it to the electricity industry, the technologies morphed into a single "concept" that became generic. Although storage consists of many different technologies, ranging from lithium-based, flow-based, and sodium-based batteries, all the way to mechanical systems such as flywheels and traditional systems such as pumped hydro and compressed air energy storage systems (CAES), industry experts began to consider them as one solution. Gone were the subtleties of technology differences - as well as any limits to the potential of a specific technology type. With this perspective, storage was lauded as the "Holy Grail" of new technologies, offering immense promise for the industry. Proponents began to contemplate how it could enhance backup power, balancing of the system, and become a ubiquitous component of our smart energy future.

Another key aspect of advanced storage was that the new technologies offered more capability than traditional battery systems. While traditional (lead-acid) storage offered a very limited number of full discharges, the new technologies could accommodate multiple discharges and thousands of full cycles. This realization spurred testing in which the technologies demonstrated and proved themselves in the field and resulted in a new set of possibilities and applications, including a myriad of potential uses and unprecedented technology applications.

The storage adaptation process accelerated as grid needs started to change as well. The desire for cleaner generation raised the prospect of installing large amounts of variable renewable resources on the grid. The pace hastened first from the wind sector - which saw a five-fold increase in wind deployments in the two years following passage of the federal Energy Policy Act of 2005. Installation of solar photovoltaics marked the next big driver, accelerating as the falling technology cost showed promise of reaching grid parity. Smart grids and future grids bring an uncommon set of requirements and technologies as well. Generally, as the amount of variable resources on the grid increases, they create new challenges to maintaining grid operations and potentially new use cases for storage.

Figure 1 - California’s Timeline for Storage Procurement

Figure 1 - California’s Timeline for Storage Procurement

Advanced storage experts began to map technologies according to specific tasks where the technology could excel. That was a crucial step. Experts stopped looking at energy storage as a solution looking for problem to solve and recognized it as a solution to particular and essential energy problems. This perspective resonates today: In a 2015 global pulse survey on renewable integration conducted by DNV GL, 66 percent of respondents ranked energy storage in their top three most important factors for integrating a high share of renewables (scoring well ahead of options such as smart grids and regulatory changes). One respondent noted that a power system with 70 percent renewables would be "science fiction" without storage.

Beyond Modeling and Valuation

At this stage of development, energy storage research has centered on the modeling side of the equation. As advanced storage was applied in earnest to utility-scale applications, from 2005 to 2010, grid operators began to ask a new set of questions. Could the "technology" solve the issues that our modernizing and evolving electricity grid would be facing? What were the effects on grid operations of extensive penetration of variable renewables? Was storage the answer to mitigating that? Was storage a better solution for supplying regulation or spinning reserve? Most of the focus at this stage addressed the natural skepticism with storage. Did the emerging technologies have the characteristics necessary to perform specific applications? Was the technology economically viable for the applications?

Hence, during this period, energy storage experts focused on ways to model the technology's unique capabilities. California ISO, the California Energy Commission (CEC) and others used tools such as DNV GL's KERMIT model to assess the impact of larger percentages of variable renewable devices on the grid. ERCOT described its experience in the May 2014 Public Utilities Fortnightly article, "Big Wind Comes to the Big Oil State." Some called 2013 the "year of storage valuation tools," as a number of organizations and the DOE's National Labs created economic valuation tools for storage. The models revealed both the challenges our future grid would create for operators, as well as confirming that technologies such as storage could solve them.

State and federal agencies formed programs with charters to accelerate the deployment of storage onto their grids. Non-profits including the New York Battery and Energy Storage Technology (NY-BEST) and the California Energy Storage Alliance (CESA) and state agencies including the California Energy Commission (CEC) and the New York State Energy Research and Development Authority (NYSERDA) helped. They introduced new applications and advocated for the peak shaving potential, demand-response, dispatchable capabilities of the technologies. National Labs continued to advance and push the technologies forward with programs such as the DOE's ARPA-E CHARGES program, which helps move emerging storage technologies into practical applications, and even advanced the potential deployments into areas such as microgrids by both modeling and then demonstrating the technologies in working labs. As the cost of some of the technologies continued to fall, stakeholders even contemplated a future where large storage systems would act as peakers, allowing cleaner advanced storage systems to replace services traditionally provided by dirtier peaker plants. Even as consensus grew around the need for flexibility in future grids, storage seemed be demonstrating its ability to provide it.

California: A Tipping Point

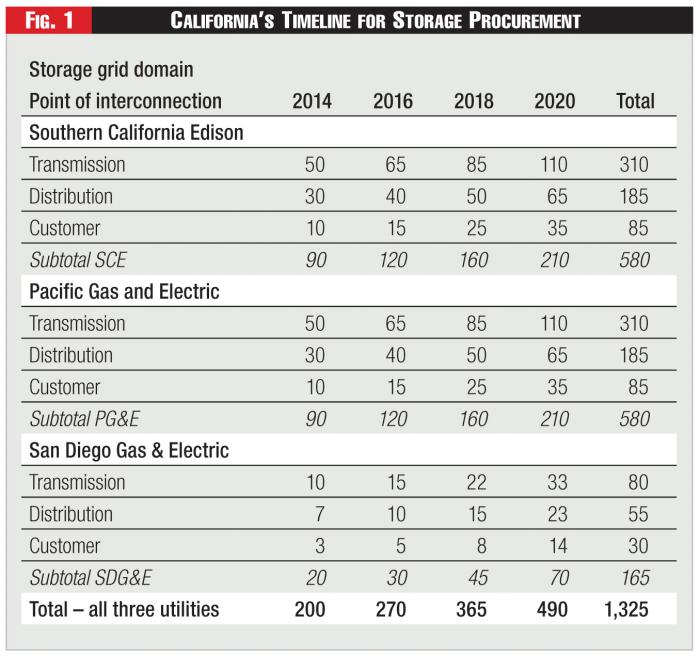

In October 2013, the California Public Utilities Commission - having armed itself with a transparent process for evaluating storage's ability to help meet its renewable energy targets and strategy tools to assess the technology's economic viability - voted 5-0 to mandate adoption of 1.325 GW of storage over a seven-year period (by 2020) on the combined systems of the state's three investor-owned electric utilities. (Calif. PUC Decision 13-10-040, Oct. 17, 2013.)

Though this event in itself did not shift storage to a state of mass deployment, it dramatically reduced the skepticism that had dogged advanced storage throughout the period of modeling and demonstration projects. From that point on, the discussion was no longer whether or if storage was going to be deployed on our system, but rather when and how storage was going to be adopted. Figure 1 illustrates the CPUC's storage targets over a seven-year period to accelerate adoption into the grid.

The year 2013 marked a sea change for energy storage adoption. In 2013 and 2014, utilities issued more RFPs (request for proposals) and announcements for megawatts of storage than in the past 30 years combined. The Independent Electricity System Operator (IESO) and Ontario Power Authority (OPA) announced an RFP in March 2014 for 50 MW of energy storage in Ontario. Hawaiian Electric Company issued an RFP for 60 to 200 MW of energy storage to integrate and meet its renewable goals for Oahu. Both Southern California and New York sought storage systems to help cover peak loads due to the decommissioning of nuclear plants.

The California energy storage ruling had other significant components as well as the targeted adoption amount. For the first time, "rate-basing" of storage systems was allowed. Half of the 1.325 GW in the California ruling was to be designated as utility owned. This spurred even more advancement into new areas of storage, as well as new initiatives. The ruling propelled utilities to examine the potential role of advanced energy storage in their systems. In November 2014, for example, Oncor Energy proposed adopting 5 GW of storage systems across Texas, worth $5.3 billion, to improve the efficiency and reliability of the state's power grid.

Dealing with Extended Lifetimes

This recent surge of activity was not limited simply to wholesale applications where "power" (short duration) storage devices were beginning to thrive. Utilities, both vertically integrated and transmission and distribution utilities, began examining the technologies as well. In such applications, where the focus was on reliability and protection of the feeders and networks, different needs arose and spurred interest in "energy" (long duration) technologies. Though most of renewable integration and ancillary service applications could be covered by power devices, other applications were beginning to emerge around reliability, peak shaving, and innovative packaging by combining storage with solar systems. That gave rise to the need of longer durations of discharge, hence longer duration technologies. A variety of different companies, like General Electric (with its Durathon Battery), EOS technology, Aquion, UniEnergy and Enervault started introducing "energy" devices to help fill this growing market niche. This shift demonstrated that the question was no longer which technology would eventually emerge as the winner, but how many winning technologies would emerge. The future market of storage would not be dominated by a single technology.

The appeal of longer duration applications - thinking in terms of multiple hours of duration for storage - was because of a growing interest in emerging grid needs for peak shaving and reliability. Solar prices were decreasing rapidly, causing a surge in interest for combined solar/storage applications. The motivation behind this combination had come not from the need to integrate storage to the grid, but rather to extend the ability of self-generated power to times when the sun sets - or in times of outages, to create a system that could produce power even absent gas and electricity infrastructure.

Nevertheless, even as new technologies had entered into the market, expanding the list of potential applications for storage, the surge in utility interest and deployment introduced another concept into storage deployment - extended project lifetimes. Heretofore, industry debate had focused on the ability of technologies to perform an application and on questions like whether to use a power device or an energy device and how to map a device's characteristics to the applications requirements. But that was yesterday. Solar projects today count on 20-year life cycles. And utility deployments now are often viewed against 15-year horizons. For an organization adopting the technology or financing a project, what will it mean to operate a system for 10 or 15 years?

Utility Scale Challenges

Over the past two years, utilities have taken concrete actions and launched large-scale energy storage deployments, propelling storage first from a modeling concept to a "proving" phase, and now to an instantaneous deployment phase. In November 2014, Southern California Edison announced winners in its 250-MW storage procurement. Hawaiian Electric Company announced in September 2014 that it was close to selecting the vendors from among the sixty who responded to the RFP for up to 200 MW of storage. Other utilities in California are also making progress. Immediately, new challenges arose - centered on the impact of subjecting storage devices to long-term, multi-year operations. We have seen examples of systems performing in roles for regulation and demonstrations occurring at many sites in the United States. However, in some cases, the cost associated with operating a system over "years" has not been well vetted, nor is such information easily accessible to the third-party entities that are now expected to respond to the surge of proposals for utility-scale storage systems.

When a technology operates in the "demonstration" phase of its lifecycle, success is often defined as the project achieving continuous operation for a two- to-three-year period and showing that the device could perform its intended and advertised application. However, with the deployments that are being seen in the market today, other issues are rising to the surface. How long can the devices really last before replacement? What is required to maintain a nameplate capacity over a 10-year or 15-year period? This question cannot be answered in the lab over a two-week period. Nor is it just an "it would be helpful to know the answer" type problem. Issues like overhaul and maintenance raise additional questions - particularly for a 20-MW project that designed to perform more than one application.

As an energy storage technology enters into a deployment phase, its projects may start looking and acting like large-scale generation projects. Where adopters of the technology previously focused on the initial capital cost of the project, now they must consider the costs of operating over the long term. For a project financier contemplating an investment in a storage project, it becomes critical to understand what happens to the device over time.

Life-Cycle Valuation

Utilities, grid operators, regulators, vendors, consultants, and consumers have all played a role in pushing storage out of the lab and onto the grid - assessing the performance of devices against the necessary applications and creating tools to assess the economic value of storage. Now that storage has "left the lab," stakeholders need more answers and more tools to support their ongoing use. Stakeholders need to know how these technologies will degrade over decades and how a device degrades because of a duty cycle or multiple duty cycles. Utility scale storage adopters, developers, and project financiers will face many new questions as they select applications storage systems for solar-storage applications, back-up power or deferral. The answers they need are not readily available in today's marketplace.

In the absence of direct data, the utility industry can leverage automotive industry studies on the long-term operational characteristics of lithium technologies. However, the automotive application is different. Utility scale applications are much bigger, typically 50 MW as compared to 50 kW for an automotive use case. Nor can a utility readily pull up to a station and swap out a battery in 10 minutes if one module starts to underperform. The consequences of failure at the utility scale are much greater, so the urgency to examine, test, and model these issues is much greater as well.

As storage projects roll out, the stakeholders that are building, financing and operating the systems need tools to examine actual costs and potential replacement costs over the 10-year or 15-year life cycle of battery operation. DNV GL and National Labs are collaboratively examining the impact of long-term battery operation from the perspective both of duty cycle and of years of operation. New tools like DNV GL's Battery XT aim to yield answers by assessing these issues, comparing a specific technology against a specific duty cycle over specified years of operation.

The financial impact on long-term operation of the devices is so important because the developers that are expected to be installing and deploying these advanced storage systems are going to be installing multi-MW systems - either as aggregated devices coupled together or as distributed devices connected to create a distributed "bulk" application - and they must have an understanding of what happens to the devices over time. Most third-party developers do not have a tradition of working with battery technologies; rather, they have a tradition of working with gas turbines, reciprocating engines, solar systems, and wind farms. The dollars invested are just as large, but the understanding of what happens after 10 years, after long-term maintenance and engine overhauls come into play, starts to take on new meaning. How many hours does the longest operating battery have? How many years has the longest battery been operating?

The storage industry is just now beginning to get some answers for lithium technologies because, as stated, those devices have a history and data from the automotive and maritime industries, and from some early utility-scale projects. However, the portfolio of utility-scale storage systems is not just comprised of lithium technologies. There are flow batteries, sodium-based batteries, variations on lithium chemistry, and as mentioned previously, unique operating applications that may have a device performing multiple applications during a day or week.

The ramifications of what is often affectionately called the "known unknowns" are that overhaul and maintenance costs rise over time, as more uncertainty is introduced to the long-term operational profile of the project. That may reflect actual replacement cost, or it may simply be risk factors and safety margins being introduced into the pricing of a storage system. However, if the cost is prohibitive, and is a result of the lack of information on the outer years of operation of a large system, then the risk can be reduced with tools being developed today.

Complexity and Promise

Battery and energy storage systems are not merely a derivative of a solar or larger generator project. The factors with storage, as we've seen in modeling their operation, can be a little more complex and encompass a few more factors that need to be taken into consideration. These factors have not created a wall or barrier for storage just yet, but it does behoove the industry to recognize that storage is no longer a technology in the lab, but that it is getting set for deployment. Now is not the time to reboot and consider if all the modeling and evaluations are complete. Deployment introduces a whole new set of requirements and needs, such as technology reviews, information to support the independent engineering studies that will need to be completed, and finally, understanding the long-term operating cost of the devices and being able to inform third-party entities that will be responsible for deploying these systems.

Energy storage has advanced rapidly, leaving the lab and entering a phase of deployment on the grid. Storage's advancements are a result of its promise as well as the tireless support of industry stakeholders who modeled, tested, evaluated and demonstrated the technology. The utility industry should celebrate, as the long- anticipated promise of energy storage stands ready to deliver. Today, even as applications have been vetted for all parts of the grid - generation, transmission, distribution and end use - this success is introducing a whole new set of challenges.

© Can Stock Photo Inc. / sumkinn, antishock